Tyson Foods 2012 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2012 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

65

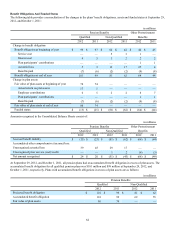

Net Periodic Benefit Cost

Components of net periodic benefit cost for pension and postretirement benefit plans recognized in the Consolidated Statements of

Income are as follows:

in millions

Pension Benefits Other Postretirement

Qualified Non-Qualified Benefits

2012 2011 2010 2012 2011 2010 2012 2011 2010

Service cost $ — $ — $ — $ 5 $ 3 $ 3 $ 1 $ — $ 1

Interest cost 455322222

Expected return on plan assets (6) (6) (6) — — — — — —

Amortization of prior service cost — — — 1 1 1 (1)(1)(1)

Recognized actuarial loss, net 3 3 1 1 — — 24 1 —

Net periodic benefit cost $ 1 $ 2 $ — $ 10 $ 6 $ 6 $ 26 $ 2 $ 2

As of September 29, 2012, the amounts expected to be reclassified into earnings within the next 12 months related to net periodic

benefit cost for the qualified and non-qualified pensions are $3 million and $3 million, respectively.

Assumptions

Weighted average assumptions are as follows:

Pension Benefits Other Postretirement

Qualified Non-Qualified Benefits

2012 2011 2010 2012 2011 2010 2012 2011 2010

Discount rate to determine net

periodic benefit cost 4.53% 5.06% 6.00% 4.75% 5.50% 6.00% 4.09% 4.50% 5.71%

Discount rate to determine

benefit obligations 4.02% 4.53% 5.06% 4.23% 4.75% 5.50% 3.66% 4.09% 4.50%

Rate of compensation increase N/A N/A N/A 3.50% 3.50% 3.50% N/A N/A N/A

Expected return on plan assets 6.37% 7.79% 7.80% N/A N/A N/A N/A N/A N/A

To determine the expected return on plan assets assumption, we first examined historical rates of return for the various asset classes.

We then determined a long-term projected rate-of-return based on expected returns over the next five to 10 years.

Our discount rate assumptions used to account for pension and other postretirement benefit plans reflect the rates at which the benefit

obligations could be effectively settled. These were determined using a cash flow matching technique whereby the rates of a yield

curve, developed from high-quality debt securities, were applied to the benefit obligations to determine the appropriate discount rate.

We have three other postretirement benefit plans which are all healthcare related. Two of these plans, which benefit obligations totaled

$26 million at September 29, 2012, were not impacted by healthcare cost trend rates as they consist of fixed annual payments. The

remaining plan, which benefit obligation was $38 million at September 29, 2012, covers retirees who do not yet qualify for Medicare

and utilized an assumed healthcare cost trend rate of 8%. A one-percentage point change in assumed healthcare cost trend rate would

have an approximate $4 million impact on the postretirement benefit obligation.