Tyson Foods 2012 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2012 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

29

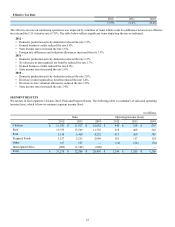

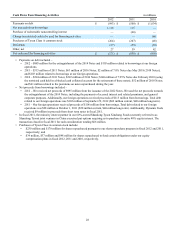

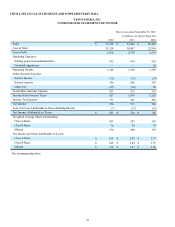

Liquidity in millions

Commitments

Expiration Date Facility

Amount

Outstanding Letters of

Credit under Revolving

Credit Facility (no

draw downs) Amount

Borrowed Amount

Available

Cash and cash equivalents $ 1,071

Revolving credit facility August 2017 $ 1,000 $ 38 $ — $ 962

Total liquidity $ 2,033

• The revolving credit facility supports our short-term funding needs and letters of credit. The letters of credit issued under this

facility are primarily in support of workers’ compensation insurance programs and derivative activities.

• Our 2013 Notes may be converted to Class A stock early during any fiscal quarter in the event our Class A stock trades at or

above $21.96 for at least 20 trading days during a period of 30 consecutive trading days ending on the last trading day of the

preceding fiscal quarter. In this event, the note holders may require us to pay outstanding principal in cash, which totaled $458

million at September 29, 2012. Any conversion premium would be paid in shares of Class A stock. The conditions for early

conversion were not met in our fourth quarter of fiscal 2012, and thus, the notes may not be converted in our first quarter of

fiscal 2013. On and after July 15, 2013, until the close of business on the second scheduled trading day immediately preceding

the maturity date, which is October 15, 2013, holders may convert their notes at any time, regardless of the foregoing

circumstances. Due to the early conversion option regardless of conversion conditions beginning in July 2013, we have

recorded the 2013 Notes balance of $458 million and remaining discount of $22 million as Current debt in our Consolidated

Balance Sheets at September 29, 2012. Should the holders exercise their early conversion option, we would use current cash

on hand and/or cash flow from operations for principal payments. We presently plan to use current cash on hand and/or cash

flows from operations for payment on the 2013 Notes not converted early upon maturity.

• At September 29, 2012, approximately 29% of our cash is held in the international accounts of our foreign subsidiaries.

Generally, we do not rely on the foreign cash as a source of funds to support our ongoing domestic liquidity needs, but rather

we manage our worldwide cash requirements by reviewing available funds among our foreign subsidiaries and the cost

effectiveness with which those funds can be accessed. The repatriation of cash balances from certain of our subsidiaries could

have adverse tax consequences or be subject to regulatory capital requirements; however, those balances are generally

available without legal restrictions to fund ordinary business operations. Our U.S. income taxes, net of applicable foreign tax

credits, have not been provided on undistributed earnings of foreign subsidiaries. Our intention is to reinvest these earnings

permanently or to repatriate the earnings only when it is tax effective to do so.

• Our current ratio was 1.91 to 1 and 2.01 to 1 at September 29, 2012, and October 1, 2011, respectively.

Capital Resources

Credit Facility

Cash flows from operating activities and current cash on hand are our primary sources of liquidity for funding debt service, capital

expenditures, dividends and share repurchases. We also have a revolving credit facility, with a committed maximum capacity of $1.0

billion, to provide additional liquidity for working capital needs, letters of credit and a source of financing for growth opportunities.

As of September 29, 2012, we had outstanding letters of credit totaling $38 million issued under this facility, none of which were

drawn upon, which left $962 million available for borrowing. Our revolving credit facility is funded by a syndicate of 43 banks, with

commitments ranging from $0.3 million to $90 million per bank. The syndicate includes bank holding companies that are required to

be adequately capitalized under federal bank regulatory agency requirements.

Capitalization

To monitor our credit ratings and our capacity for long-term financing, we consider various qualitative and quantitative factors. We

monitor the ratio of our debt to our total capitalization as support for our long-term financing decisions. At September 29, 2012, and

October 1, 2011, the ratio of our debt-to-total capitalization was 28.7% and 27.7%, respectively. For the purpose of this calculation,

debt is defined as the sum of current and long-term debt. Total capitalization is defined as debt plus Total Shareholders’ Equity. Our

ratio of debt to our total capitalization increased in fiscal 2012 primarily resulting from the net increase in our debt balance from

issuing the $1.0 billion 2022 Notes and extinguishing the $810 million 2014 Notes.