Tyson Foods 2012 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2012 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

57

Undesignated positions

In addition to our designated positions, we also hold forward and option contracts for which we do not apply hedge accounting. These

include certain derivative instruments related to commodities price risk, including grains, livestock, energy, foreign currency risk and

interest rate risk. We mark these positions to fair value through earnings at each reporting date. We generally do not enter into

undesignated positions beyond 18 months.

The objective of our undesignated grains, livestock and energy commodity positions is to reduce the variability of cash flows

associated with the forecasted purchase of certain grains, energy and livestock inputs to our production processes. We also enter into

certain forward sales of boxed beef and boxed pork and forward purchases of cattle and hogs at fixed prices. The fixed price sales

contracts lock in the proceeds from a future sale and the fixed cattle and hog purchases lock in the cost. However, the cost of the

livestock and the related boxed beef and boxed pork market prices at the time of the sale or purchase could vary from this fixed price.

As we enter into fixed forward sales of boxed beef and boxed pork and forward purchases of cattle and hogs, we also enter into the

appropriate number of livestock options and futures positions to mitigate a portion of this risk. Changes in market value of the open

livestock options and futures positions are marked to market and reported in earnings at each reporting date, even though the

economic impact of our fixed prices being above or below the market price is only realized at the time of sale or purchase. These

positions generally do not qualify for hedge treatment due to location basis differences between the commodity exchanges and the

actual locations when we purchase the commodities.

We have a foreign currency cash flow hedging program to hedge portions of forecasted transactions denominated in foreign

currencies, primarily with forward and option contracts, to protect against the reduction in value of forecasted foreign currency cash

flows. Our undesignated foreign currency positions generally would qualify for cash flow hedge accounting. However, to reduce

earnings volatility, we normally will not elect hedge accounting treatment when the position provides an offset to the underlying

related transaction that impacts current impacts.

The objective of our undesignated interest rate swap is to manage interest rate risk exposure on a floating-rate bond. Our interest rate

swap agreement effectively modifies our exposure to interest rate risk by converting a portion of the floating-rate bond to a fixed rate

basis for the first five years, thus reducing the impact of the interest-rate changes on future interest expense. This interest rate swap

does not qualify for hedge treatment due to differences in the underlying bond and swap contract interest-rate indices.

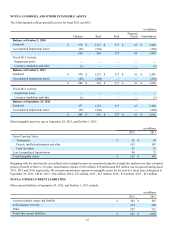

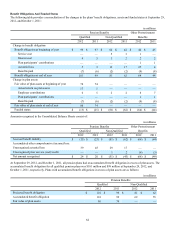

We had the following aggregate outstanding notional values related to our undesignated positions (in millions, except soy meal tons):

Metric September 29, 2012 October 1, 2011

Commodity:

Corn Bushels 19 17

Soy Meal Tons 1,200 174,600

Soy Oil Pounds 17 13

Live Cattle Pounds 68 72

Lean Hogs Pounds 108 19

Foreign Currency United States dollars $ 165 $ 110

Interest Rate Average monthly notional debt $ 27 $ 39

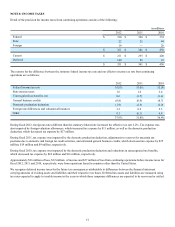

The following table sets forth the pretax impact of the undesignated derivative instruments on the Consolidated Statements of Income

(in millions):

Consolidated

Statements of Income

Classification

Gain/(Loss)

Recognized

in Earnings

2012 2011 2010

Derivatives not designated as hedging instruments:

Commodity contracts Sales $ (10) $ 20 $ 27

Commodity contracts Cost of Sales 51 (2) (20)

Foreign exchange contracts Other Income/Expense — (3) (5)

Interest rate contracts Interest Expense — — 1

Total $ 41 $ 15 $ 3