Tyson Foods 2012 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2012 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

55

NOTE 11: DERIVATIVE FINANCIAL INSTRUMENTS

Our business operations give rise to certain market risk exposures mostly due to changes in commodity prices, foreign currency

exchange rates and interest rates. We manage a portion of these risks through the use of derivative financial instruments, primarily

futures and options, to reduce our exposure to commodity price risk, foreign currency risk and interest rate risk. Forward contracts on

various commodities, including grains, livestock and energy, are primarily entered into to manage the price risk associated with

forecasted purchases of these inputs used in our production processes. Foreign exchange forward contracts are entered into to manage

the fluctuations in foreign currency exchange rates, primarily as a result of certain receivable and payable balances. We also

periodically utilize interest rate swaps to manage interest rate risk associated with our variable-rate borrowings.

Our risk management programs are periodically reviewed by our Board of Directors’ Audit Committee. These programs are monitored

by senior management and may be revised as market conditions dictate. Our current risk management programs utilize industry-

standard models that take into account the implicit cost of hedging. Risks associated with our market risks and those created by

derivative instruments and the fair values are strictly monitored, using Value-at-Risk and stress tests. Credit risks associated with our

derivative contracts are not significant as we minimize counterparty concentrations, utilize margin accounts or letters of credit, and

deal with credit-worthy counterparties. Additionally, our derivative contracts are mostly short-term in duration and we generally do

not make use of credit-risk-related contingent features. No significant concentrations of credit risk existed at September 29, 2012.

We recognize all derivative instruments as either assets or liabilities at fair value in the Consolidated Balance Sheets, with the

exception of normal purchases and normal sales expected to result in physical delivery. The accounting for changes in the fair value

(i.e., gains or losses) of a derivative instrument depends on whether it has been designated and qualifies as part of a hedging

relationship and the type of hedging relationship. For those derivative instruments that are designated and qualify as hedging

instruments, we designate the hedging instrument based upon the exposure being hedged (i.e., fair value hedge, cash flow hedge, or

hedge of a net investment in a foreign operation). We qualify, or designate, a derivative financial instrument as a hedge when contract

terms closely mirror those of the hedged item, providing a high degree of risk reduction and correlation. If a derivative instrument is

accounted for as a hedge, depending on the nature of the hedge, changes in the fair value of the instrument either will be offset against

the change in fair value of the hedged assets, liabilities or firm commitments through earnings, or be recognized in other

comprehensive income (loss) (OCI) until the hedged item is recognized in earnings. The ineffective portion of an instrument’s change

in fair value is recognized in earnings immediately. We designate certain forward contracts as follows:

• Cash Flow Hedges – include certain commodity forward and option contracts of forecasted purchases (i.e., grains) and certain

foreign exchange forward contracts.

• Fair Value Hedges – include certain commodity forward contracts of forecasted purchases (i.e., livestock).

• Net Investment Hedges – include certain foreign currency forward contracts of permanently invested capital in certain foreign

subsidiaries.

Cash flow hedges

Derivative instruments, such as futures and options, are designated as hedges against changes in the amount of future cash flows

related to procurement of certain commodities utilized in our production processes. We do not purchase forward and option

commodity contracts in excess of our physical consumption requirements and generally do not hedge forecasted transactions beyond

18 months. The objective of these hedges is to reduce the variability of cash flows associated with the forecasted purchase of those

commodities. For the derivative instruments we designate and qualify as a cash flow hedge, the effective portion of the gain or loss on

the derivative is reported as a component of OCI and reclassified into earnings in the same period or periods during which the hedged

transaction affects earnings. Gains and losses representing hedge ineffectiveness are recognized in earnings in the current period.

Ineffectiveness related to our cash flow hedges was not significant during fiscal 2012, 2011 and 2010.

We had the following aggregated notional values of outstanding forward and option contracts accounted for as cash flow hedges (in

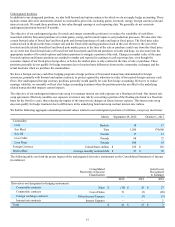

millions, except soy meal tons):

Metric September 29, 2012 October 1, 2011

Commodity:

Corn Bushels 12 6

Soy Meal Tons 164,700 82,300

Foreign Currency United States dollar $ 80 $ 75

As of September 29, 2012, the net amounts expected to be reclassified into earnings within the next 12 months are pretax gains of $18

million related to grain and pretax losses of $2 million related to foreign currency. During fiscal 2012, 2011 and 2010, we did not

reclassify significant pretax gains/losses into earnings as a result of the discontinuance of cash flow hedges due to the probability the

original forecasted transaction would not occur by the end of the originally specified time period or within the additional period of

time allowed by generally accepted accounting principles.