Tyson Foods 2012 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2012 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

19

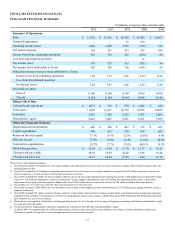

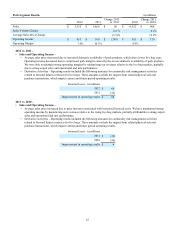

FISCAL 2013 OUTLOOK

Our continued capital investment in our businesses, strong liquidity and reduced interest expense has put us in a strong position as we

begin a challenging fiscal 2013. The drought conditions in the summer of 2012 reduced grain supplies, which will result in higher

input costs as well as increased costs for cattle and hog producers. USDA data indicates in fiscal 2013 overall domestic protein

production (chicken, beef, pork and turkey) is expected to decrease 2% compared to fiscal 2012, which should continue to support

improved pricing. The following is a summary of the fiscal 2013 outlook for each of our segments, as well as an outlook on sales,

capital expenditures, net interest expense, debt and liquidity, share repurchases and dividends:

• Chicken – Current USDA data shows U.S. chicken production will be down slightly in fiscal 2013. Due to the reduced crop

supply, we expect higher grain costs in fiscal 2013 compared to fiscal 2012 of approximately $600 million. However, the

capital investment and significant operational, mix and pricing improvements we have made in our Chicken segment have

better positioned us to adapt to rising grain prices. For fiscal 2013, we anticipate our Chicken segment will remain profitable,

but could be below our normalized range of 5.0%-7.0%.

• Beef – We expect to see a reduction of industry fed cattle supplies of 2-3% in fiscal 2013 as compared to fiscal 2012. Although

we generally expect adequate supplies in regions we operate our plants, there may be periods of imbalance of fed cattle supply

and demand. We anticipate beef exports will remain strong. For fiscal 2013, we believe our Beef segment will remain

profitable, but could be below our normalized range of 2.5%-4.5%.

• Pork – We expect industry hog supplies in fiscal 2013 to be flat compared to fiscal 2012 and pork exports to remain strong.

For fiscal 2013, we believe our Pork segment will be in or above our normalized range of 6.0%-8.0%.

• Prepared Foods – We expect operational improvements and increased pricing to offset increased raw material costs. Because

many of our sales contracts are formula based or shorter-term in nature, we are typically able to offset rising input costs

through increased pricing. For fiscal 2013, we believe our Prepared Foods segment will remain in its normalized range of

4.0%-6.0%.

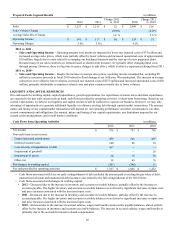

• Sales – We expect fiscal 2013 sales to increase to approximately $35 billion mostly resulting from price increases related to

decreases in domestic availability of protein and rising raw material costs.

• Capital Expenditures – Our preliminary capital expenditures plan for fiscal 2013 is approximately $550 million. The reduction

in planned capital expenditures from fiscal 2012 is primarily a result of an anticipated rise in working capital needs in fiscal

2013. Once we gain more visibility into our working capital needs, or should forecasted conditions change, we may raise our

capital expenditures target. We will continue to make significant investments in our production facilities for high return

operational efficiencies, other profit improvement projects and development of our foreign operations.

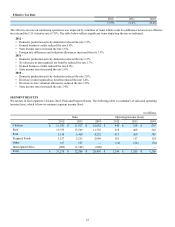

• Net Interest Expense – We expect fiscal 2013 net interest expense will approximate $140 million.

• Debt and Liquidity – We do not have any significant maturities of debt due until October 2013. We may use our available cash

to repurchase notes when available at attractive rates. Total liquidity at September 29, 2012, was $2.0 billion, well above our

goal to maintain liquidity in excess of $1.2 billion.

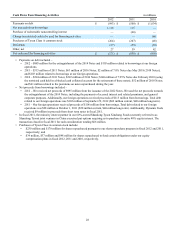

• Share Repurchases – We expect to continue repurchasing shares under our share repurchase plan. In fiscal 2012, we

repurchased 12.5 million shares for approximately $230 million. As of September 29, 2012, 35.2 million shares remain

authorized for repurchases. The timing and extent to which we repurchase shares will depend upon, among other things, our

working capital needs, market conditions, liquidity targets, our debt obligations and regulatory requirements.

• Dividends – On November 15, 2012, the Board of Directors declared a special dividend of $0.10 per share on our Class A

common stock and $0.09 per share on our Class B common stock. Additionally, the Board increased the quarterly dividend

previously declared on August 3, 2012, to $0.05 per share on our Class A common stock and $0.045 per share on our Class B

common stock. Both the special dividend and the increased quarterly dividend are payable on December 14, 2012, to

shareholders of record at the close of business on November 30, 2012. The Board also declared a quarterly dividend of $0.05

per share on our Class A common stock and $0.045 per share on our Class B common stock, payable on March 31, 2013, to

shareholders of record at the close of business on March 1, 2013.