Tyson Foods 2012 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2012 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

61

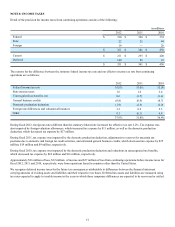

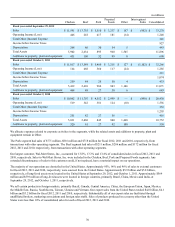

(in millions) September 29, 2012 October 1, 2011

Amortized

Cost Basis Fair

Value Unrealized

Gain/(Loss) Amortized

Cost Basis Fair

Value Unrealized

Gain/(Loss)

Available for Sale Securities:

Debt Securities:

U.S. Treasury and Agency $ 26 $ 27 $ 1 $ 33 $ 34 $ 1

Corporate and Asset-Backed (a) 64 66 2 54 56 2

Redeemable Preferred Stock 20 20 — 27 27 —

Equity Securities:

Common Stock and Warrants 9 7 (2) 9 7 (2)

(a) At September 29, 2012, and October 1, 2011, the amortized cost basis for Corporate and Asset-Backed debt securities had been

reduced by accumulated other than temporary impairments of $2 million and $3 million, respectively.

Unrealized holding gains (losses), net of tax, are excluded from earnings and reported in OCI until the security is settled or sold. On a

quarterly basis, we evaluate whether losses related to our available-for-sale securities are temporary in nature. Losses on equity

securities are recognized in earnings if the decline in value is judged to be other than temporary. If losses related to our debt securities

are determined to be other than temporary, the loss would be recognized in earnings if we intend, or more likely than not will be

required, to sell the security prior to recovery. For debt securities in which we have the intent and ability to hold until maturity, losses

determined to be other than temporary would remain in OCI, other than expected credit losses which are recognized in earnings. We

consider many factors in determining whether a loss is temporary, including the length of time and extent to which the fair value has

been below cost, the financial condition and near-term prospects of the issuer and our ability and intent to hold the investment for a

period of time sufficient to allow for any anticipated recovery. During fiscal 2012, 2011 and 2010, we recognized no other than

temporary impairments in earnings. No other than temporary losses were deferred in OCI as of September 29, 2012, and October 1,

2011.

Deferred Compensation Assets: We maintain non-qualified deferred compensation plans for certain executives and other highly

compensated employees. Investments are maintained within a trust and include money market funds, mutual funds and life insurance

policies. The cash surrender value of the life insurance policies is invested primarily in mutual funds. The investments are recorded at

fair value based on quoted market prices and are included in Other Assets in the Consolidated Balance Sheets. We classify the

investments which have observable market prices in active markets in Level 1 as these are generally publicly-traded mutual funds. The

remaining deferred compensation assets are classified in Level 2, as fair value can be corroborated based on observable market data.

Realized and unrealized gains (losses) on deferred compensation are included in earnings.

Assets and Liabilities Measured at Fair Value on a Nonrecurring Basis

In addition to assets and liabilities that are recorded at fair value on a recurring basis, we record assets and liabilities at fair value on a

nonrecurring basis. Generally, assets are recorded at fair value on a nonrecurring basis as a result of impairment charges. During fiscal

2010, we recorded a $29 million charge to fully impair an immaterial Chicken segment reporting unit’s goodwill. We utilized a

discounted cash flow analysis that incorporated unobservable Level 3 inputs. We did not have any other significant measurements of

assets or liabilities at fair value on a nonrecurring basis subsequent to their initial recognition.

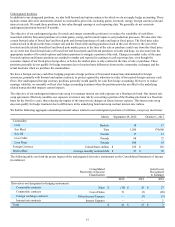

Other Financial Instruments

Fair value of our debt is principally estimated using Level 2 inputs based on quoted prices for those or similar instruments. Fair value

and carrying value for our debt are as follows (in millions):

September 29, 2012 October 1, 2011

Fair

Value Carrying

Value Fair

Value Carrying

Value

Total Debt $ 2,596 $ 2,432 $ 2,334 $ 2,182

Concentrations of Credit Risk

Our financial instruments exposed to concentrations of credit risk consist primarily of cash and cash equivalents and accounts

receivable. Our cash equivalents are in high quality securities placed with major banks and financial institutions. Concentrations of

credit risk with respect to receivables are limited due to the large number of customers and their dispersion across geographic areas.

We perform periodic credit evaluations of our customers’ financial condition and generally do not require collateral. At September 29,

2012, and October 1, 2011, 17.1% and 16.5%, respectively, of our net accounts receivable balance was due from Wal-Mart Stores, Inc.

No other single customer or customer group represented greater than 10% of net accounts receivable.