Tyson Foods 2004 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2004 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

39

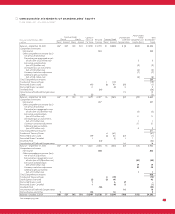

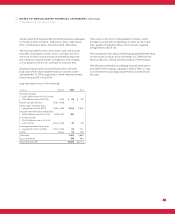

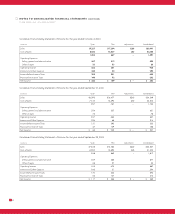

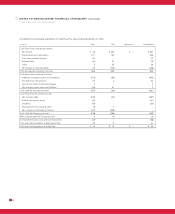

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

for the closing of the Berlin operation in accordance with SFAS No. 146

and SFAS No. 144. At October 2, 2004, $9 million of obligations under

grower contracts and $3 million of other closing costs had been

paid. Additionally, a $2 million decrease to the original accrual was

recorded in the fourth quarter of fiscal 2004.

In the first quarter of fiscal 2003, the Company recorded $47 million

of costs related to the closing of its Stilwell, Oklahoma, and

Jacksonville, Florida, plants that included $26 million of costs related

to closing the plants and $21 million of estimated impairment charges

for assets to be disposed. The costs related to closing the plants

include $17 million for estimated liabilities for the resolution of the

Company’s obligations under grower contracts, and $9 million of

other related costs associated with the closing of the plants including

plant clean-up costs and employee termination benefits. The

Company accounted for the closing of the Stilwell, Oklahoma, and

Jacksonville, Florida, operations in accordance with Emerging Issues

Task Force No. 94-3, “Liability Recognition for Certain Employee

Termination Benefits and Other Costs to Exit an Activity” (EITF 94-3)

and SFAS No. 144. The costs are reflected in the Chicken segment as

a reduction of operating income and included in the Consolidated

Statements of Income in other charges. As of October 2, 2004, the

remaining accrual balance was $1 million, as $16 million of obliga-

tions under grower contracts and $13 million of other closing costs

had been paid. Additionally, a $4 million increase to the original

accrual amount was recorded in the fourth quarter of fiscal 2004.

No material adjustments to the total accrual are anticipated at

this time.

In the fourth quarter of fiscal 2002, the Company recorded $26 million

of costs related to the restructuring of its live swine operations

that consists of $21 million of estimated liabilities for resolution of

Company obligations under producer contracts and $5 million of

other related costs associated with this restructuring, including

lagoon and pit closure costs and employee termination benefits.

In the fourth quarter of 2004, the Company recorded an addi-

tional reserve of $6 million related to lagoon and pit closures costs.

At October 2, 2004, the remaining accrual balance was $18 million,

as $6 million of obligations under grower contracts and $8 million

of other related costs had been paid. The Company is accounting for

the restructuring of its live swine operations in accordance with

EITF 94-3 and SFAS No. 144. No material adjustments to the total

accrual are anticipated at this time.

In August 2002, the Company made the decision to capitalize on

the strong recognition of the Tyson brand by expanding the Tyson

brand to beef and pork. Thus, in the fourth quarter of fiscal 2002,

the Company recorded a write-down of $27 million related to the

discontinuation of the Thomas E. Wilson brand. This amount is

reflected in the Prepared Foods segment as a reduction to operating

income and included on the Consolidated Statements of Income in

other charges.

NOTE FIVE : BSE-RELATED CHARGES

On December 23, 2003, the U.S. Department of Agriculture (USDA)

announced that a single case of BSE had been diagnosed in a

Washington State dairy cow. The effect on the Company’s Beef

segment caused by that announcement, along with the decision of

various countries to restrict imports of U.S. beef products, resulted

in the Company recording BSE-related pretax charges of approximately

$61 million in fiscal 2004. These charges were included in cost of

sales and primarily related to the decline in value of finished product

inventory destined for international markets, whether in-transit,

located at the shipping ports or located within domestic storage,

as well as live cattle inventory and open futures positions. No material

adjustments were made subsequent to the initial BSE-related accruals

recorded in first quarter of fiscal 2004, and none are anticipated in

the future.

NOTE SIX : ALLOWANCE FOR DOUBTFUL ACCOUNTS

At October 2, 2004, and September 27, 2003, the allowance for

doubtful accounts was $11 million and $16 million, respectively.

NOTE SEVEN : FINANCIAL INSTRUMENTS

The Company purchases certain commodities in the course of normal

operations such as corn, soybeans, livestock and natural gas. As part

of the Company’s on-going commodity risk management activities,

the Company uses derivative financial instruments, primarily futures

and swaps, to reduce its exposure to various market risks related to

these purchases. Generally, contract terms of a financial instrument

qualifying as a hedge instrument closely mirror those of the hedged

item, providing a high degree of risk reduction and correlation.

Contracts that are designated and highly effective at meeting the

risk reduction and correlation criteria are recorded using hedge

accounting, as defined by Statement of Financial Accounting

Standards No. 133, “Accounting for Derivative Instruments and

Hedging Activities” (SFAS No. 133), as amended. If a derivative

instrument is a hedge, as defined by SFAS No. 133, changes in the

fair value of the instrument will either be offset against the change

in fair value of the hedged assets, liabilities or firm commitments

through earnings or recognized in other comprehensive income

(loss) until the hedged item is recognized in earnings. The ineffective

portion of an instrument’s change in fair value will be immediately

recognized in earnings as a component of cost of sales.