Tyson Foods 2004 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2004 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

36

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

The Company is a purchaser of certain

commodities, such as corn, soybeans, livestock and natural gas in

the course of normal operations. The Company uses derivative

financial instruments to reduce its exposure to various market risks.

Generally, contract terms of a hedge instrument closely mirror those

of the hedged item, providing a high degree of risk reduction and

correlation. Contracts that are designated and highly effective at

meeting the risk reduction and correlation criteria are recorded using

hedge accounting, as defined by Statement of Financial Accounting

Standards No. 133, “Accounting for Derivative Instruments and Hedging

Activities” (SFAS No. 133), as amended. If a derivative instrument is

a hedge, as defined by SFAS No. 133, depending on the nature of the

hedge, changes in the fair value of the instrument will either be offset

against the change in fair value of the hedged assets, liabilities or firm

commitments through earnings or recognized in other comprehen-

sive income (loss) until the hedged item is recognized in earnings.

The ineffective portion of an instrument’s change in fair value will

be immediately recognized in earnings as a component of cost of

sales. Instruments the Company holds as part of its risk manage-

ment activities that do not meet the criteria for hedge accounting,

as defined by SFAS No. 133, as amended, are marked to fair value

with unrealized gains or losses reported currently in earnings. The

Company generally does not hedge anticipated transactions

beyond 12 months.

The Company recognizes revenue when title

and risk of loss are transferred to customers, which is generally upon

delivery based upon terms of sale. Revenue is recognized as the net

amount estimated to be received after deducting estimated amounts

for discounts, trade allowances and product terms.

There are a variety of legal proceedings pending

or threatened against the Company. Accruals are recorded when it

is probable that a liability has been incurred and the amount of the

liability can be reasonably estimated based on current law, progress

of each case, opinions and views of legal counsel and other advisers,

the Company’s experience in similar matters and management’s

intended response to the litigation. These amounts, which are not

discounted and are exclusive of claims against third parties, are

adjusted periodically as assessment efforts progress or additional

information becomes available. The Company expenses amounts

for administering or litigating claims as incurred. Accruals for legal

proceedings are included in other current liabilities in the accom-

panying balance sheets.

Freight expense associated with products shipped

to customers is recognized in cost of products sold.

Advertising and promotion

expenses are charged to operations in the period incurred. Advertising

and promotion expenses for fiscal 2004, 2003 and 2002 were

$465 million, $504 million and $396 million, respectively.

The consolidated financial statements are prepared

in conformity with accounting principles generally accepted in the

United States, which require management to make estimates and

assumptions that affect the amounts reported in the consolidated

financial statements and accompanying notes. Actual results could

differ from those estimates.

In

December 2004, the FASB issued Statement of Financial Accounting

Standards No. 151, “Inventory Costs” (SFAS No. 151). SFAS No. 151

requires abnormal amounts of inventory costs related to idle facility,

freight handling and wasted material expenses to be recognized

as current period charges. Additionally, SFAS No. 151 requires that

allocation of fixed production overheads to the costs of conversion

be based on the normal capacity of the production facilities.

The standard is effective for fiscal years beginning after June 15,

2005. The Company believes the adoption of SFAS No. 151 will not

have a material impact on its consolidated financial statements.

On October 22, 2004, the President signed into law the American

Jobs Creation Act of 2004 (the Bill). The Company is currently in

the process of evaluating the Bill.

In March 2004, the Emerging Issues Task Force (EITF) reached a

consensus on Issue No. 03-6, “Participating Securities and the

Two-Class Method under FASB Statement No. 128, Earnings per Share.”

This issue involves the computation of earnings per share for

companies that have multiple classes of common stock or have issued

securities other than common stock that participate in dividends

with common stock (participating securities). The EITF concluded

that companies having participating securities are required to apply

the two-class method to compute earnings per share. The two-class

method is an earnings allocation method under which earnings per

share is calculated for each class of common stock and participating

security considering both dividends declared (or accumulated) and

participation rights in undistributed earnings as if all such earnings

had been distributed during the period. The Company adopted

EITF Issue No. 03-6 in the fourth quarter of fiscal 2004. As required

by EITF Issue No. 03-6, prior period earnings per share have been

restated as follows:

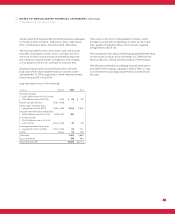

2003 2002

Earnings per share as previously reported

Basic $0.98 $1.10

Diluted 0.96 1.08

Earnings per share, restated in accordance

with EITF Issue No. 03-6

Class A Basic 1.00 1.13

Class B Basic 0.90 1.02

Diluted 0.96 1.08