Tyson Foods 2004 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2004 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

27

MANAGEMENT’S DISCUSSION AND ANALYSIS (CONTINUED)

Among the factors that cause actual results and experiences to

differ from the anticipated results and expectations expressed in

such forward-looking statements are the following: (i) fluctuations

in the cost and availability of raw materials, such as live cattle, live

swine or feed grains; (ii) market conditions for finished products,

including the supply and pricing of alternative proteins, and the

demand for alternative proteins; (iii) risks associated with effectively

evaluating derivatives and hedging activities; (iv) access to foreign

markets together with foreign economic conditions, including

currency fluctuations and import/export restrictions; (v) outbreak

of a livestock disease which could have an effect on livestock

owned by the Company, the availability of livestock for purchase

by the Company, or the Company’s ability to access certain markets;

(vi) successful rationalization of existing facilities, and the operating

efficiencies of the facilities; (vii) changes in the availability and rela-

tive costs of labor and contract growers; (viii) issues related to food

safety, including costs resulting from product recalls, regulatory

compliance and any related claims or litigation; (ix) adverse results

from litigation; (x) risks associated with leverage, including cost

increases due to rising interest rates or changes in debt ratings or

outlook; (xi) changes in regulations and laws (both domestic and

foreign), including changes in accounting standards, environmental

laws and occupational, health and safety laws; (xii) the ability of the

Company to make effective acquisitions, and successfully integrate

newly acquired businesses into existing operations; (xiii) effective-

ness of advertising and marketing programs; and (xiv) the effect of,

or changes in, general economic conditions.

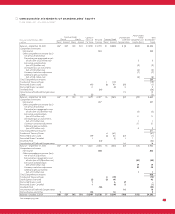

Market risks relating to the Company’s operations result primarily

from changes in commodity prices, interest rates and foreign exchange

rates, as well as credit risk concentrations. To address certain of these

risks, the Company enters into various derivative transactions as

described below. If a derivative instrument is a hedge, as defined

by SFAS No. 133, as amended, depending on the nature of the hedge,

changes in the fair value of the instrument will be either offset against

the change in fair value of the hedged assets, liabilities or firm

commitments through earnings, or recognized in other comprehen-

sive income (loss) until the hedged item is recognized in earnings. The

ineffective portion of an instrument’s change in fair value, as defined

by SFAS No. 133, as amended, will be immediately recognized in earn-

ings as a component of cost of sales. Additionally, the Company holds

certain positions, primarily in grain and livestock futures which do

not meet the criteria for SFAS No. 133 hedge accounting. These posi-

tions are marked to fair value and the unrealized gains and losses

are reported in earnings at each reporting date. The changes in market

value of derivatives used in the Company’s risk management activi-

ties surrounding inventories on hand or anticipated purchases of

inventories are recorded in cost of sales. The changes in market value

of derivatives used in the Company’s risk management activities

surrounding forward sales contracts are recorded in sales.

The sensitivity analyses presented on the following page are the

measures of potential losses of fair value resulting from hypotheti-

cal changes in market prices related to commodities. Sensitivity

analyses do not consider the actions management may take to

mitigate the Company’s exposure to changes, nor do they consider

the effects that such hypothetical adverse changes may have on

overall economic activity. Actual changes in market prices may

differ from hypothetical changes.

The Company is a purchaser of certain commodities,

such as corn, soybeans, livestock and natural gas in the course of

normal operations. The Company uses commodity futures to reduce

the effect of changing prices and as a mechanism to procure the

underlying commodity. However, as the commodities underlying

the Company’s derivative financial instruments can experience

significant price fluctuations, any requirement to mark-to-market

the positions that have not been designated or do not qualify as

hedges under SFAS No. 133 could result in volatility in the Company’s

results of operations. Generally, contract terms of a hedge instrument

closely mirror those of the hedged item providing a high degree of

risk reduction and correlation. Contracts that are designated and

highly effective at meeting this risk reduction and correlation criteria

are recorded using hedge accounting. The following table presents

a sensitivity analysis resulting from a hypothetical change of 10%

in market prices as of October 2, 2004, and September 27, 2003,

respectively, on fair value of open positions. The fair value of such

positions is a summation of the fair values calculated for each

commodity by valuing each net position at quoted futures prices.

The market risk exposure analysis includes hedge and non-hedge

positions. The underlying commodities hedged have a correlation to

price changes of the derivative positions such that the values of the

commodities hedged based on differences between commitment

prices and market prices and the value of the derivative positions

used to hedge these commodity obligations are inversely correlated.

The following sensitivity analysis reflects an inverse impact on

earnings for changes in the fair value of open positions for livestock

and natural gas and a direct impact on earnings for changes in the

fair value of open positions for grain.