Starwood 2004 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2004 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

STARWOOD HOTELS & RESORTS WORLDWIDE, INC.

AND STARWOOD HOTELS & RESORTS

NOTES TO FINANCIAL STATEMENTS Ì (Continued)

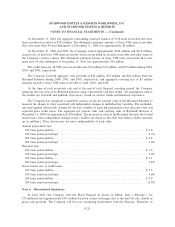

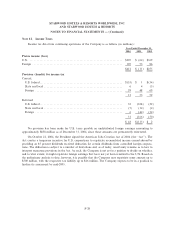

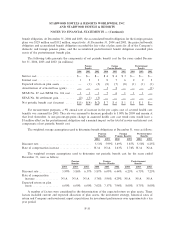

Note 7. Goodwill and Intangible Assets

The changes in the carrying amount of goodwill for the year ended December 31, 2004 are as follows (in

millions):

Vacation

Hotel Ownership

Segment Segment Total

Balance at January 1, 2004 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $1,869 $241 $2,110

Acquisitions ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 22 Ì 22

Settlement of tax contingency ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (3) Ì (3)

Purchase price adjustment ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 22 Ì 22

Cumulative translation adjustment ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11 Ì 11

Asset dispositions ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (5) Ì (5)

Balance at December 31, 2004 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $1,916 $241 $2,157

Intangible assets consisted of the following (in millions):

December 31,

2004 2003

Trademarks and trade names ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $232 $226

Management and franchise agreementsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 177 168

Other ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 64 59

473 453

Accumulated amortization ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (86) (75)

$387 $378

Amortization expense of $15 million, $13 million and $13 million, respectively, related to intangible

assets with Ñnite lives was recorded during the years ended December 31, 2004, 2003 and 2002. Amortization

expense relating to these assets is expected to be at least $14 million in each of the Ñscal years 2005 through

2011.

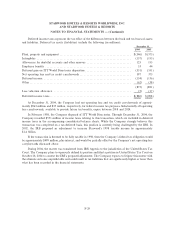

Note 8. Other Assets

Other assets include notes receivable, net of $295 million and $275 million at December 31, 2004 and

2003, respectively, primarily related to the Ñnancing of VOIs (as discussed in Note 5. Notes Receivable

Securitizations and Sales).

Contractual Obligations. On December 30, 2003, the Company together with Lehman Brothers

Holdings Inc. (""Lehman Brothers''), announced the acquisition of all of the outstanding senior debt

(approximately $1.3 billion), at a discount, of Le Meridien Hotels and Resorts Ltd. (""Le Meridien''). The

approximate $200 million investment is represented by a high yield junior participation interest. As part of this

investment, the Company entered into an agreement with Lehman Brothers whereby they would negotiate

with the Company on an exclusive basis towards a recapitalization of Le Meridien. The exclusivity period

expired in early April 2004 although negotiations with Lehman Brothers are continuing. While negotiations

are continuing, there can be no assurance that transaction agreements will be entered into or a transaction

consummated and if consummated what the terms and form of such a transaction would be.

F-25