Starwood 2004 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2004 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

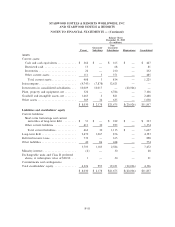

STARWOOD HOTELS & RESORTS WORLDWIDE, INC.

AND STARWOOD HOTELS & RESORTS

NOTES TO FINANCIAL STATEMENTS Ì (Continued)

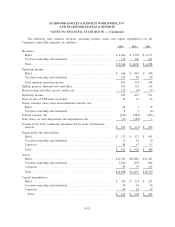

Savannah. In July 2002, the Company acquired a 49% interest in the Westin Savannah Harbor Resort

and Spa in connection with the restructuring of the indebtedness of that property. An unrelated party holds an

additional 49% interest in the property. The remaining 2% is held by Troon. Troon invested in the project on a

pari-passu basis and manages the golf course at the Westin Savannah. The unrelated third party negotiated the

terms of the golf management agreement with Troon, and approved the terms of its equity interest, and

therefore, the Company believes the arrangements are on an arms-length basis.

Aircraft Lease. In February 1998, the Company leased a Gulfstream III Aircraft (""GIII'') from Star

Flight LLC, an aÇliate of Starwood Capital. The term of the lease was one year and automatically renews for

one-year terms until either party terminates the lease upon 90 days' written notice. The rent for the aircraft,

which was set at approximately 90% of fair market value at the time (based on two estimates from unrelated

third parties), is (i) a monthly payment of 1.25% of the lessor's total costs relating to the aircraft

(approximately $123,000 at the beginning of the lease with this amount increasing as additional costs are

incurred by the lessor), plus (ii) $300 for each hour that the aircraft is in use. The lease was revised eÅective

January 1, 2004. Under the revised terms, the monthly lease payment is equal to (i) 1% of the fair market

value of the aircraft as determined by an independent appraisal in February 2005, with the fair market value of

the aircraft to be determined annually, plus (ii) $300 for each hour that the aircraft is in use. The term of the

new lease agreement is for one year and it automatically renews for one-month terms unless either party

terminates the lease upon 90 days' written notice. The amount paid in 2004 in excess of the revised amount

due (approximately $658,000) will be refunded by Star Flight LLC upon execution of the amended lease.

Payments to Star Flight LLC were $1,724,000 (before the refunded amount disclosed above), $1,865,000 and

$2,052,000 in 2004, 2003 and 2002, respectively. Starwood Capital has used the GIII as well as the

Gulfstream IV Aircraft (""GIV'') operated by the Company. For use of the GIII, Star Flight LLC relieves the

Company of lease payments for the days the plane is used and reimburses it for costs of operating the aircraft.

For use of the GIV, Starwood Capital pays a charter rate that is at least equal to the amount the Company

would have received from an unaÇliated third party through the Company's charter agent, net of commis-

sions. Lease relief and reimbursed operating costs were approximately $208,000, $52,000 and $161,000 for

Ñscal 2004, 2003 and 2002, respectively.

Other

The Company on occasion made loans to employees, including executive oÇcers prior to August 23,

2002, principally in connection with home purchases upon relocation. As of December 31, 2004, approxi-

mately $5.6 million in loans to approximately 15 employees was outstanding of which approximately

$4.4 million were non-interest bearing home loans. Home loans are generally due Ñve years from the date of

issuance or upon termination of employment and are secured by a second mortgage on the employee's home.

Executive oÇcers receiving home loans in connection with relocation were Robert F. Cotter, President and

Chief Operating OÇcer, in June 2001 (original balance of $600,000), David K. Norton, Executive Vice

President of Human Resources, in July 2000 (original balance of $500,000), and Theodore W. Darnall,

President, Real Estate Group, in 1996 and 1998 (original balance of $750,000 ($150,000 bridge loan in 1996

and $600,000 home loan in 1998), of which $600,000 was repaid in August 2003). As a result of the

acquisition of ITT Corporation in 1998, restricted stock awarded to Messrs. Sternlicht and Darnall in 1996

vested at a price for tax purposes of $53 per Share. This amount was taxable at ordinary income rates. By late

1998, the value of the stock had fallen below the amount of income tax owed. In order to avoid a situation in

which the executives could be required to sell all of the Shares acquired by them to cover income taxes, in

April 1999 the Company made interest-bearing loans at 5.67% to Messrs. Sternlicht and Darnall of

approximately $1,222,000 and $416,000 respectively, to cover the taxes payable. Mr. Darnall's loan was repaid

in 2004. Accrued interest on Mr. Sternlicht's loan at December 31, 2004 is approximately $396,000. The note

and all associated accumulated interest become due on their tenth anniversary.

F-45