Starwood 2004 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2004 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

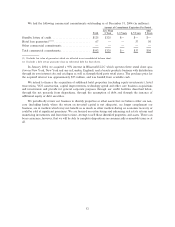

Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

In limited instances, we seek to reduce earnings and cash Öow volatility associated with changes in

interest rates and foreign currency exchange rates by entering into Ñnancial arrangements intended to provide

a hedge against a portion of the risks associated with such volatility. We continue to have exposure to such

risks to the extent they are not hedged.

Interest rate swap agreements are the primary instruments used to manage interest rate risk. At

December 31, 2004, we had two outstanding long-term interest rate swap agreements under which we pay

variable interest rates and receive Ñxed interest rates. At December 31, 2004, we had no interest rate swap

agreements under which we pay a Ñxed rate and receive a variable rate. The following table sets forth the

scheduled maturities and the total fair value of our debt portfolio:

Expected Maturity or Total Fair

Transaction Date Total at Value at

At December 31, December 31, December 31,

2005 2006 2007 2008 2009 Thereafter 2004 2004

Liabilities

Fixed rate (in millions)ÏÏÏÏÏÏÏÏÏÏ $480 $379 $754 $22 $432 $1,607 $3,674 $4,024

Average interest rate ÏÏÏÏÏÏÏÏÏÏÏÏ 6.25%

Floating rate (in millions) ÏÏÏÏÏÏÏ $139 $521 $ 90 $ 5 $ 9 $ 4 $ 768 $ 768

Average interest rate ÏÏÏÏÏÏÏÏÏÏÏÏ 4.12%

Interest Rate Swaps

Fixed to variable (in millions) ÏÏÏÏ $ Ì $ Ì $ Ì $Ì $ Ì $ 300 $ 300

Average pay rate ÏÏÏÏÏÏÏÏÏÏÏÏÏ 6.72%

Average receive rate ÏÏÏÏÏÏÏÏÏÏ 7.88%

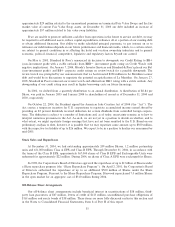

We use foreign currency hedging instruments to manage exposure to foreign currency exchange rate

Öuctuations. The gains or losses on the hedging instruments are largely oÅset by gains or losses on the

underlying asset or liability, and consequently, a sudden signiÑcant change in foreign currency exchange rates

would not have a material impact on future net income or cash Öows of the hedged item. We monitor our

foreign currency exposure on a monthly basis to maximize the overall eÅectiveness of our foreign currency

hedge positions. Changes in the fair value of hedging instruments are classiÑed in the same manner as changes

in the underlying assets or liabilities due to Öuctuations in foreign currency exchange rates. At December 31,

2004, the notional amount of our open foreign exchange hedging contracts protecting the value of our foreign

currency denominated assets and liabilities was approximately $562 million, which includes a hedge on a

portion of the principal amount of the Le Meridien investment. A hypothetical 10% change in the spot

currency exchange rates would result in an increase or decrease of approximately $61 million in the fair value

of the hedges at December 31, 2004, which would be oÅset by an opposite eÅect on the related underlying net

asset or liability.

We enter into a derivative Ñnancial arrangement to the extent it meets the objectives described above,

and we do not engage in such transactions for trading or speculative purposes.

See Note 18. Derivative Financial Instruments in the notes to Ñnancial statements Ñled as part of this

Joint Annual Report and incorporated herein by reference for further description of derivative Ñnancial

instruments.

Item 8. Financial Statements and Supplementary Data.

The Ñnancial statements and supplementary data required by this Item are included in Item 15 of this

Joint Annual Report and are incorporated herein by reference.

36