Red Lobster 2012 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2012 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Darden

Darden Restaurants, Inc. 2012 Annual Report 29

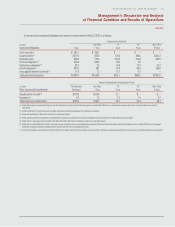

with lives that approximate the maturity of the plan benefits. At May 27, 2012,

our discount rate was 4.4 percent and 4.5 percent, respectively, for our defined

benefit and postretirement benefit plans. The expected long-term rate of return

on plan assets and health care cost trend rates are based upon several factors,

including our historical assumptions compared with actual results, an analysis of

current market conditions, asset allocations and the views of leading financial

advisers and economists. Our assumed expected long-term rate of return on plan

assets for our defined benefit plan was 9.0 percent for each of the fiscal years

reported. At May 27, 2012, the expected health care cost trend rate assumed

for our postretirement benefit plan for fiscal 2013 was 7.7 percent. The rate

gradually decreases to 5.0 percent through fiscal 2022 and remains at that level

thereafter. We made contributions of approximately $22.2 million, $12.9 million

and $0.4 million in fiscal years 2012, 2011 and 2010, respectively, to our defined

benefit pension plan to maintain its targeted funded status as of each annual

valuation date.

The expected long-term rate of return on plan assets component of our

net periodic benefit cost is calculated based on the market-related value of plan

assets. Our target asset fund allocation is 40 percent U.S. equities, 35 percent

high-quality, long-duration fixed-income securities, 20 percent international

equities, 5 percent real estate securities. We monitor our actual asset fund

allocation to ensure that it approximates our target allocation and believe that

our long-term asset fund allocation will continue to approximate our target

allocation. In developing our expected rate of return assumption, we have

evaluated the actual historical performance and long-term return projections of

the plan assets, which give consideration to the asset mix and the anticipated

timing of the pension plan outflows. We employ a total return investment

approach whereby a mix of equity and fixed-income investments are used to

maximize the long-term return of plan assets for what we consider a prudent

level of risk. Our historical 10-year, 15-year and 20-year rates of return on

plan assets, calculated using the geometric method average of returns,

are approximately 7.8 percent, 8.0 percent and 9.4 percent, respectively,

as of May 27, 2012.

We have recognized net actuarial losses, net of tax, as a component of

accumulated other comprehensive income (loss) for the defined benefit plans and

postretirement benefit plan as of May 27, 2012 of $87.4 million and $1.9 million,

respectively. These net actuarial losses represent changes in the amount of the

projected benefit obligation and plan assets resulting from differences in the

assumptions used and actual experience. The amortization of the net actuarial

loss component of our fiscal 2013 net periodic benefit cost for the defined

benefit plans and postretirement benefit plan is expected to be approximately

$8.8 million and $0.0 million, respectively.

We believe our defined benefit and postretirement benefit plan assumptions

are appropriate based upon the factors discussed above. However, other assump-

tions could also be reasonably applied that could differ from the assumptions

used. A quarter-percentage point change in the defined benefit plans’ discount

rate and the expected long-term rate of return on plan assets would increase

or decrease earnings before income taxes by $0.7 million and $0.5 million,

respectively. A quarter-percentage point change in our postretirement benefit

plan discount rate would increase or decrease earnings before income taxes by

$0.1 million. A one-percentage point increase in the health care cost trend rates

would increase the accumulated postretirement benefit obligation (APBO) by

$6.5 million at May 27, 2012 and the aggregate of the service cost and interest

cost components of net periodic postretirement benefit cost by

$0.5 million for fiscal 2012. A one-percentage point decrease in the health care

cost trend rates would decrease the APBO by $5.1 million at May 27, 2012 and

the aggregate of the service cost and interest cost components of net periodic

postretirement benefit cost by $0.4 million for fiscal 2012. These changes in

assumptions would not significantly impact our funding requirements. We expect

to contribute approximately $17.5 million to $19.5 million to our defined benefit

pension plans and approximately $1.0 million to our postretirement benefit plan

during fiscal 2013.

On July 12, 2012, we entered into an agreement to acquire Yard House

for $585.0 million in an all-cash transaction. After the acquisition, Yard House

will be a wholly-owned subsidiary of Darden. The transaction has been approved

by our Board of Directors and is subject to the satisfaction of customary closing

conditions, including, among others, the expiration or termination of the applicable

waiting periods under the Hart-Scott-Rodino Antitrust Improvements Act of

1976. The acquisition is expected to be completed early in the second quarter

of fiscal 2013.

With the exception of the pending Yard House acquisition discussed above,

we are not aware of any trends or events that would materially affect our capital

requirements or liquidity. We believe that our internal cash-generating capabilities,

the potential issuance of unsecured debt securities under our shelf registration

statement and short-term commercial paper should be sufficient to finance our

capital expenditures, including the Yard House acquisition, debt maturities, stock

repurchase program and other operating activities through fiscal 2013.

OFF-BALANCE SHEET ARRANGEMENTS

We are not a party to any off-balance sheet arrangements that have, or are

reasonably likely to have, a current or future material effect on our financial

condition, changes in financial condition, sales or expenses, results of operations,

liquidity, capital expenditures or capital resources.

FINANCIAL CONDITION

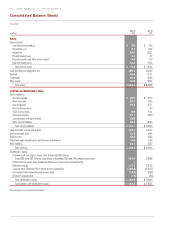

Our total current assets were $757.6 million at May 27, 2012, compared

with $663.8 million at May 29, 2011. The increase was primarily due to higher

inventory levels related to the timing of inventory purchases as a result of our

strategy to take ownership of our inventory earlier in the supply chain to ensure

a more secure and efficient supply of inventory to our restaurants.

Our total current liabilities were $1.77 billion at May 27, 2012, compared

with $1.29 billion at May 29, 2011. The increase was primarily due to an increase

in short-term debt related to our use of short-term financing to repurchase

shares of our common stock, capital expenditures, purchase of inventory and the

reclassification of long-term debt maturing within the next year.