Red Lobster 2012 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2012 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Darden

18 Darden Restaurants, Inc. 2012 Annual Report

This discussion and analysis below for Darden Restaurants, Inc. (Darden, the

Company, we, us or our) should be read in conjunction with our consolidated

financial statements and related financial statement notes found elsewhere in this

report. We operate on a 52/53 week fiscal year, which ends on the last Sunday

in May. Fiscal 2012, 2011 and 2010 each consisted of 52 weeks of operation.

OVERVIEW OF OPERATIONS

Our business operates in the full-service dining segment of the restaurant

industry, primarily in the United States. At May 27, 2012, we operated 1,994

Red Lobster®, Olive Garden®, LongHorn Steakhouse®, The Capital Grille®,

Bahama Breeze®, Seasons 52®, Eddie V’s Prime Seafood® and Wildfish Seafood

Grille® restaurants in the United States and Canada. Through subsidiaries, we

own and operate all of our restaurants in the United States and Canada, except

for three restaurants located in Central Florida that are owned by joint ventures

and managed by us. None of our restaurants in the United States or Canada are

franchised. As of May 27, 2012, we also had 28 restaurants outside the United

States and Canada operated by independent third parties pursuant to area

development and franchise agreements, including 5 LongHorn Steakhouse

restaurants in Puerto Rico, 22 Red Lobster restaurants in Japan and

1 Red Lobster restaurant in Dubai.

On November 14, 2011, we completed the acquisition of eight Eddie V’s

Prime Seafood restaurants and three Wildfish Seafood Grille restaurants (collec-

tively Eddie V’s) and all related assets and net working capital for $58.5 million

in cash. The results of operations from Eddie V’s, which are not material, are

included in our consolidated financial statements from the date of acquisition.

Our mission is to be the best in full-service dining, now and for generations.

We believe we can achieve this goal by continuing to build on our strategy to be

a multi-brand restaurant growth company, which is grounded in:

•Brandrelevance;

•Brandsupport;

•Avibrantbusinessmodel;

•Competitivelysuperiorleadership;and

•Aunifying,motivatingculture.

We seek to increase profits by leveraging our fixed and semi-fixed costs

with sales from new restaurants and increased guest traffic and sales at existing

restaurants. To evaluate our operations and assess our financial performance, we

monitor a number of operating measures, with a special focus on two key factors:

•Same-restaurantsales–whichisayear-over-yearcomparisonofeach

period’s sales volumes for restaurants open at least 16 months, including

recently acquired restaurants, regardless of when the restaurants were

acquired;and

•Restaurantearnings–whichisrestaurant-levelprofitability(restaurant

sales, less restaurant-level cost of sales, marketing and depreciation).

Increasing same-restaurant sales can improve restaurant earnings because

these incremental sales provide better leverage of our fixed and semi-fixed

restaurant-level costs. A restaurant brand can generate same-restaurant sales

increases through increases in guest traffic, increases in the average guest

check, or a combination of the two. The average guest check can be impacted by

menu price changes and by the mix of menu items sold. For each restaurant

brand, we gather daily sales data and regularly analyze the guest traffic counts

and the mix of menu items sold to aid in developing menu pricing, product offer-

ings and promotional strategies. We view same-restaurant guest counts as a

measure of the long-term health of a restaurant brand, while increases in average

check and menu mix may contribute more significantly to near-term profitability.

We focus on balancing our pricing and product offerings with other initiatives to

produce sustainable same-restaurant sales growth.

We compute same-restaurant sales using restaurants open at least

16 months because this period is generally required for new restaurant sales

levels to normalize. Sales at newly opened restaurants generally do not make a

significant contribution to profitability in their initial months of operation due to

operating inefficiencies. Our sales and expenses can be impacted significantly by

the number and timing of new restaurant openings and closings, relocation and

remodeling of existing restaurants. Pre-opening expenses each period reflect the

costs associated with opening new restaurants in current and future periods.

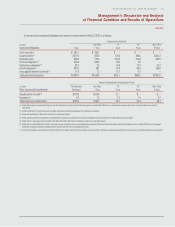

Fiscal 2012 Financial Highlights

Our sales from continuing operations were $8.00 billion in fiscal 2012 compared

to $7.50 billion in fiscal 2011. The 6.6 percent increase was primarily driven

by the addition of 89 net new company-owned restaurants plus the addition of

11 Eddie V’s purchased restaurants, and a blended same-restaurant sales

increase for Olive Garden, Red Lobster and LongHorn Steakhouse. Our blended same-

restaurant sales increase for Olive Garden, Red Lobster and LongHorn Steakhouse

of 1.8 percent compares to an increase of 1.3 percent for the Knapp-Track™

benchmark of U.S. same-restaurant sales excluding Darden. Net earnings from

continuing operations for fiscal 2012 were $476.5 million ($3.58 per diluted

share) compared with net earnings from continuing operations for fiscal 2011 of

$478.7 million ($3.41 per diluted share). Net earnings from continuing operations

for fiscal 2012 decreased 0.5 percent and diluted net earnings per share from

continuing operations increased 5.0 percent compared with fiscal 2011.

Our net losses from discontinued operations were $1.0 million ($0.01 per

diluted share) for fiscal 2012, compared with net losses from discontinued oper-

ations of $2.4 million ($0.02 per diluted share) for fiscal 2011. When combined

with results from continuing operations, our diluted net earnings per share were

$3.57 and $3.39 for fiscal 2012 and 2011, respectively.

Outlook and Strategy

On July 12, 2012, we entered into an agreement to acquire Yard House USA, Inc.

(Yard House), for $585.0 million in an all-cash transaction. The acquisition is

expected to be completed early in the second quarter of fiscal 2013. See the

subsection below entitled “Liquidity and Capital Resources” for further details.

We expect blended U.S. same-restaurant sales in fiscal 2013 to increase

between 1.0 percent and 2.0 percent for Olive Garden, Red Lobster and

LongHorn Steakhouse. Including the impact from operations of Yard House, we

expect fiscal 2013 total sales to increase between 9.0 percent and 10.0 percent

and diluted net earnings per share growth from continuing operations for fiscal

2013 to range from 5.0 percent to 9.0 percent. In fiscal 2013, exclusive of the

Yard House transaction, we expect to add approximately 100 to 110 net new

restaurants, and we expect capital expenditures will be approximately

$750 million, including approximately $15 million to $20 million in information

technology platform enhancements.