Pentax 2007 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2007 Pentax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

|

|

63

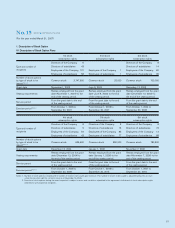

2. Valuation Method for Fair Value of Stock Options

The 6th stock subscription rights granted for the year ended March 31, 2007 are valued as follows:

Fair value of stock subscription rights is valued for each of the following exercise periods.

(a) From October 1, 2007 to September 30, 2008

(b) From October 1, 2007 to September 30, 2009

(c) From October 1, 2007 to September 30, 2010

(d) From October 1, 2007 to September 30, 2016

a. Option-pricing model used: Black–Scholes model

b. Major assumptions used:

(a) (b) (c) (d)

Stock price volatility (Note 1) 32.28% 33.91% 34.32% 37.19%

Estimated time to exercise (Note 2) 5.40 years 5.90 years 6.40 years 6.90 years

Estimated dividends (Note 3) ¥60 ¥60 ¥60 ¥60

Risk free rate (Note 4) 1.32% 1.38% 1.43% 1.49%

Notes: 1. It is based on historical volatility of stock price for the period, corresponding to the estimated time to exercise, prior to the grant date.

2. It is assumed to be exercised in the middle of the exercise period due to the lack of enough data for other reasonable estimation.

3. It is based on the actual dividends for the year ended March 31, 2006.

4. It is based on interest rates on national government bonds with maturity corresponding to the estimated time to exercise.

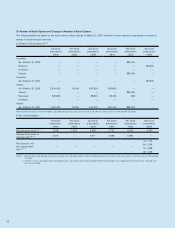

3. Estimation Methods for Number of Vested Stock Options

Only the actual number of stock options forfeited is reflected due to difficulty in estimating the number of stock options to be forfeited in

the future.

4.

Stock-based compensation expense is recorded on the consolidated statement of income for the year ended March 31, 2007 as follows:

Cost of sales ¥ 44 million

Selling, general and administrative expenses ¥123 million

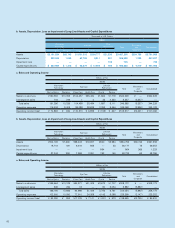

1. The Outline and Purposes of Transaction

Following the decision made by the chief executive officer of the

Company on July 28, 2006, the Company split-up its contact lens

production function and merged it into HOYA HEALTHCARE

CORPORATION, a wholly-owned subsidiary, on October 1, 2006.

The purpose of this transaction is to achieve more efficient man-

agement for the Group; HOYA HEALTHCARE CORPORATION,

which currently engages in retail of contact lens, is expected to

be able to reflect market needs more rapidly and effectively into

development and production by combining the related production

function.

2. Shares to Be Issued

No shares were to be issued in connection with this transaction,

as permitted under the Corporate Law of Japan, since HOYA

HEALTHCARE CORPORATION is a wholly-owned subsidiary of

the Company.

3. Treatment of the Company’s Stock Subscription Rights

Stock subscription rights of HOYA HEALTHCARE CORPORATION

will not be allocated to the holders of stock subscription rights of

the Company as substitutes.

4. Summary of Accounting Treatment

Since the transaction is classified as “transactions under

common control” under the “Accounting Standard for Business

Combinations,” the Company does not recognize gain/loss on

the transaction, and HOYA HEALTHCARE CORPORATION is to

record the assets and liabilities transferred at their book value

before the transaction.

No. 16 BUSINESS COMBINATIONS AND BUSINESS DIVESTITURES