Neiman Marcus 2009 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2009 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

|

|

Table of Contents

end of each fiscal year. In the third quarter of fiscal year 2010, we froze benefits offered to all remaining employees under our

Pension Plan and SERP Plan.

Significant assumptions related to the calculation of our obligations include the discount rate used to calculate the present

value of benefit obligations to be paid in the future, the expected long-term rate of return on assets held by the Pension Plan and the

health care cost trend rate for the Postretirement Plan. We review these assumptions annually based upon currently available

information, including information provided by our actuaries.

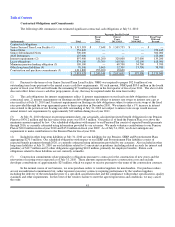

Significant assumptions utilized in the calculation of our projected benefit obligations as of July 31, 2010 and future expense

requirements for our Pension Plan, SERP Plan and Postretirement Plan, and sensitivity analysis related to changes in these

assumptions, are as follows:

Using Sensitivity Rate

Actual

Rate

Sensitivity Rate

Increase/(Decrease)

Increase in

Liability

(in millions)

Increase/

(Decrease) in

Expense

(in millions)

Pension Plan:

Discount rate 5.20% (0.25)% $ 18.4 $ 0.3

Expected long-term rate of return on plan

assets 8.00% (1.00)% N/A $ 3.3

SERP Plan:

Discount rate 5.20% (0.25)% $ 2.9 $ (0.1)

Postretirement Plan:

Discount rate 5.10% (0.25)% $ 0.6 $ 0.1

Ultimate health care cost trend rate 8.00% 1.00% $ 2.4 $ 0.1

Income Taxes. We use the asset and liability method of accounting for income taxes. Under this method, deferred tax assets

and liabilities are determined based on differences between financial reporting and tax basis of assets and liabilities and are measured

using the enacted tax rates and laws that will be in effect when the differences are expected to reverse. We are routinely under audit

by federal, state or local authorities in the area of income taxes. We regularly evaluate the likelihood of realization of tax benefits

derived from positions we have taken in various federal and state filings after consideration of all relevant facts, circumstances and

available information. For those tax benefits we believe more likely than not will be sustained, we recognize the benefit we believe is

cumulatively greater than 50% likely to be realized. To the extent we were to prevail in matters for which accruals have been

established or be required to pay amounts in excess of recorded reserves, our effective tax rate in a given financial statement period

could be materially impacted.

Recent Accounting Pronouncements

In December 2007, the FASB issued guidance that addresses the recognition and accounting for identifiable assets acquired,

liabilities assumed and non-controlling interests in business combinations. In addition, this guidance changes the accounting treatment

for certain acquisition-related items, including requirements to expense acquisition-related costs as incurred, expense restructuring

costs associated with an acquired business and recognize post-acquisition changes in tax uncertainties associated with a business

combination as a component of tax expense. These rules are to be applied prospectively to business combinations for which the

acquisition date is on or after December 15, 2008. Generally, the effect of this guidance will depend on future acquisitions. However,

the accounting for the resolution of any tax uncertainties remaining as of July 31, 2010 related to the Acquisition will be subject to the

provisions of this guidance. As to the future resolution of these tax uncertainties, we do not believe these requirements will have a

material impact on our future financial statements.

In February 2008, the FASB issued guidance that currently requires disclosure related to the fair values of nonfinancial

assets, such as intangible assets and goodwill, and nonfinancial liabilities that are recognized or disclosed at fair value in the financial

statements on a nonrecurring basis. We adopted this guidance during the first quarter of fiscal year 2010. However, the adoption of

this guidance does not currently result in additional required disclosures in our consolidated financial statements for fiscal year 2010.

In June 2009, the FASB issued guidance that establishes the Accounting Standards Codification (ASC) as the source of

authoritative accounting principles recognized by the FASB to be applied by nongovernmental entities in the preparation of financial

statements in conformity with generally accepted accounting principles. This guidance is effective for financial

47