Neiman Marcus 2009 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2009 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

|

|

Table of Contents

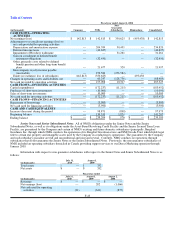

On July 12, 2010, all defendants except for the Company were dismissed without prejudice, and on August 20, 2010, this case was

refiled in the Superior Court of California for San Francisco County. This Complaint, along with a similar class action lawsuit

originally filed by Bernadette Tanguilig in 2007, alleges that the Company has engaged in various violations of the California Labor

Code and Business and Professions Code, including without limitation (1) asking employees to work "off the clock," (2) failing to

provide meal and rest breaks to its employees, (3) improperly calculating deductions on paychecks delivered to its employees, and

(4) failing to provide a chair or allow employees to sit during shifts. The plaintiffs in these matters seek certification of their case as a

class action, reimbursement for past wages and temporary, preliminary and permanent injunctive relief preventing defendant from

allegedly continuing to violate the laws cited in their complaints. We intend to vigorously defend our interests in these matters.

Currently, we cannot reasonably estimate the amount of loss, if any, arising from these matters. However, we do not currently believe

the resolution of these matters will have a material adverse impact on our financial position. We will continue to evaluate these

matters based on subsequent events, new information and future circumstances.

We are currently involved in various other legal actions and proceedings that arose in the ordinary course of business. We

believe that any liability arising as a result of these actions and proceedings will not have a material adverse effect on our financial

position, results of operations or cash flows.

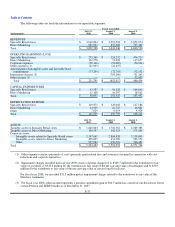

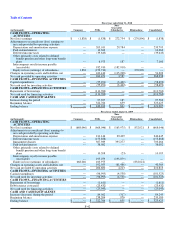

Other. We had approximately $31.1 million of outstanding irrevocable letters of credit relating to purchase commitments

and insurance and other liabilities at July 31, 2010. We had approximately $3.2 million in surety bonds at July 31, 2010 relating

primarily to merchandise imports and state sales tax and utility requirements.

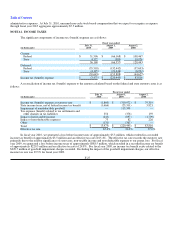

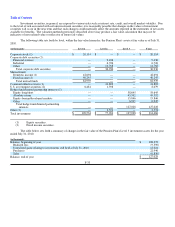

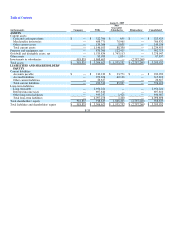

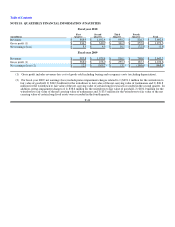

NOTE 15. ACCUMULATED OTHER COMPREHENSIVE LOSS

The following table shows the components of accumulated other comprehensive loss (amounts are recorded net of related

income taxes):

(in thousands)

July 31,

2010

August 1,

2009

Unrealized loss on financial instruments $ (17,281) $ (35,508)

Change in unfunded benefit obligations (88,993) (69,011)

Other — (68)

Total accumulated other comprehensive loss $ (106,274)$ (104,587)

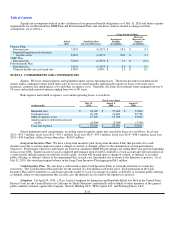

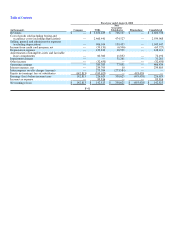

NOTE 16. SEGMENT REPORTING

We have identified two reportable segments: Specialty Retail stores and Direct Marketing. The Specialty Retail stores

segment aggregates the activities of our Neiman Marcus and Bergdorf Goodman retail stores, including Neiman Marcus Last Call

stores. The Direct Marketing segment conducts both online and print catalog operations under the Neiman Marcus, Bergdorf

Goodman and Horchow brand names. Both the Specialty Retail stores and Direct Marketing segments derive their revenues from the

sales of high-end fashion apparel, accessories, cosmetics and fragrances from leading designers, precious and fashion jewelry and

decorative home accessories.

Operating earnings (loss) for the segments include 1) revenues, 2) cost of sales, 3) direct selling, general, and administrative

expenses, 4) other direct operating expenses, 5) income from credit card program and 6) depreciation expense for the respective

segment. Items not allocated to our operating segments include those items not considered by management in measuring the assets

and profitability of our segments. These amounts include 1) corporate expenses including, but not limited to, treasury, investor

relations, legal and finance support services, and general corporate management, 2) charges related to the application of purchase

accounting adjustments made in connection with the Acquisition including amortization of intangible assets and favorable lease

commitments and other non-cash items and 3) interest expense. These items, while often related to the operations of a segment, are

not considered by segment operating management, corporate operating management and the chief operating decision maker in

assessing segment operating performance. The accounting policies of the operating segments are the same as those described in the

summary of significant accounting policies (except with respect to purchase accounting adjustments not allocated to the operating

segments).

F-36