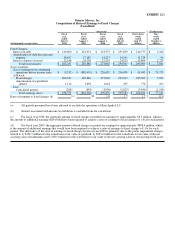

Neiman Marcus 2009 Annual Report Download - page 478

Download and view the complete annual report

Please find page 478 of the 2009 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

468 -

469

469 -

470

470 -

471

471 -

472

472 -

473

473 -

474

474 -

475

475 -

476

476 -

477

477 -

478

478 -

479

479 -

480

480 -

481

481 -

482

482 -

483

483 -

484

484 -

485

485 -

486

486 -

487

487 -

488

488 -

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

|

|

Exhibit 10.55

AMENDMENT NO. 1 TO

THE NEIMAN MARCUS GROUP, INC.

SUPPLEMENTAL EXECUTIVE RETIREMENT PLAN

(Amended and Restated Effective January 1, 2009)

Pursuant to Section 6.1 of The Neiman Marcus Group, Inc. Supplemental Executive Retirement Plan (Amended and Restated

Effective January 1, 2009) (the "Plan"), the Plan is hereby amended in the following respect only:

FIRST: Section 2.4 of the Plan is hereby amended by restatement in its entirety to read as follows:

2.4 Cessation of Accruals.

(a) Participation After December 31, 2007. A Participant who is a Grandfathered Rule of 65 Employee as of

December 31, 2007 shall continue to be a Participant under the Plan thereafter, subject to and in accordance with the terms of

the Plan; provided, however, that if a Grandfathered Rule of 65 Employee has a Termination of Employment after

December 31, 2007, such employee shall not be treated as a Grandfathered Rule of 65 Employee upon any later

reemployment by a Participating Employer. Any provision of the Plan to the contrary notwithstanding, no individual shall

become an Eligible Employee on or after January 1, 2008 who was not an Eligible Employee on December 31, 2007 and,

thus, there shall be no new Participants in the Plan on and after such date, and a Participant who is not a Grandfathered

Rule of 65 Employee shall remain a Participant in the Plan after December 31, 2007 as long as he or she is entitled to receive

a benefit under the Plan, but no additional benefit shall accrue for any Participant who is not a Grandfathered Rule of 65

Employee under the Plan after December 31, 2007, subject to the following:

(i) the amount of benefit payable under the Plan after December 31, 2007 with respect to a Participant who

is an Eligible Employee as of such date but who is not a Grandfathered Rule of 65 Employee shall be determined as

if such Participant had a Termination of Employment effective as of December 31, 2007, provided, however, that

any such Participant shall not be treated as having a Termination of Employment for purposes of determining

whether he or she has attained Normal Retirement Age until his or her actual Termination of Employment and

benefit payments shall not commence to any such Participant until payments would otherwise commence to such

Participant under the terms of the Plan; and

(ii) a Participant who is not a Grandfathered Rule of 65 Employee shall continue to be entitled to credit for

Service after December 31, 2007 for purposes of determining whether such Participant has attained the required

years of Service to vest in a benefit or to commence receiving a benefit prior to Normal Retirement Date, but not

for purposes of the calculation of the amount of such benefit.