Lexmark 2007 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2007 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

demographics, mortality rates and investment performance. Refer to Part II, Item 8, Note 14 of the Notes to

Consolidated Financial Statements for additional information relating to the Company’s pension and other

postretirement plans.

The Pension Protection Act of 2006 (“the Act”) was enacted on August 17, 2006. Most of its provisions will

become effective in 2008. The Act significantly changes the funding requirements for single-employer

defined benefit pension plans. The funding requirements will now largely be based on a plan’s calculated

funded status, with faster amortization of any shortfalls or surpluses. The Act directs the U.S. Treasury

Department to develop a new yield curve to discount pension obligations for determining the funded status

of a plan when calculating the funding requirements. The provisions of the Act are not expected to have a

material impact on the Company’s financial position, results of operations and cash flows.

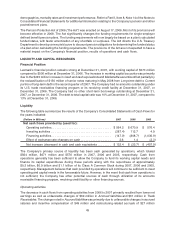

LIQUIDITY AND CAPITAL RESOURCES

Financial Position

Lexmark’s financial position remains strong at December 31, 2007, with working capital of $570 million

compared to $506 million at December 31, 2006. The increase in working capital accounts was primarily

due to the $245 million increase in Cash and cash equivalents and Marketable securities offset partially by

the reclassification of $150 million of senior notes maturing in May 2008 from Long-term debt to Current

portion of long-term debt in the second quarter of 2007. The Company had no amounts outstanding under

its U.S. trade receivables financing program or its revolving credit facility at December 31, 2007, or

December 31, 2006. The Company had no other short-term borrowings outstanding at December 31,

2007, or December 31, 2006. The debt to total capital ratio was 10% at December 31, 2007, compared to

13% at December 31, 2006.

Liquidity

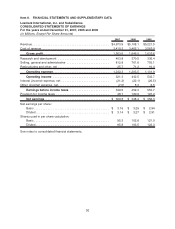

The following table summarizes the results of the Company’s Consolidated Statements of Cash Flows for

the years indicated:

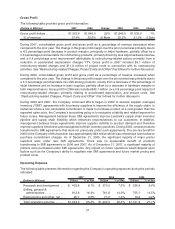

(Dollars in Millions) 2007 2006 2005

Net cash flows provided by (used for):

Operating activities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 564.2 $ 670.9 $ 576.4

Investing activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (287.4) 112.7 4.9

Financing activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (147.0) (808.7) (1,036.9)

Effect of exchange rate changes on cash . . . . . . . . . . . . . . . . . . 2.6 1.4 (2.3)

Net increase (decrease) in cash and cash equivalents . . . . . . . . $ 132.4 $ (23.7) $ (457.9)

The Company’s primary source of liquidity has been cash generated by operations, which totaled

$564 million, $671 million and $576 million in 2007, 2006 and 2005, respectively. Cash from

operations generally has been sufficient to allow the Company to fund its working capital needs and

finance its capital expenditures during these periods along with the repurchase of approximately

$0.2 billion, $0.9 billion and $1.1 billion of its Class A Common Stock during 2007, 2006 and 2005,

respectively. Management believes that cash provided by operations will continue to be sufficient to meet

operating and capital needs in the foreseeable future. However, in the event that cash from operations is

not sufficient, the Company has other potential sources of cash through utilization of its accounts

receivable financing program, revolving credit facility or other financing sources.

Operating activities

The decrease in cash flows from operating activities from 2006 to 2007 primarily resulted from lower net

earnings as well as unfavorable changes of $69 million in Accrued liabilities and $61 million in Trade

Receivables. The change noted in Accrued liabilities was primarily due to unfavorable changes in accrued

salaries and incentive compensation of $49 million and restructuring-related accruals of $27 million

45