Kohl's 2011 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2011 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

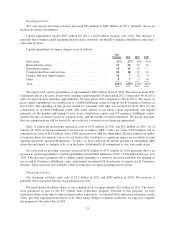

•Incremental borrowing rate—We estimate our incremental borrowing rate using treasury rates for

debt with maturities comparable to the expected lease term and our credit spread. The incremental

borrowing rate is primarily used in determining whether the lease is accounted for as an operating lease

or a capital lease. A lease is considered a capital lease if the net present value of the lease payments is

greater than 90% of the fair market value of the property. Increasing the incremental borrowing rate

decreases the net present value of the lease payments and reduces the probability that a lease will be

considered a capital lease. For leases which are recorded on our balance sheet with a related capital

lease or financing obligation, the incremental borrowing rate is also used in allocating our rental

payments between interest expense and a reduction of the outstanding obligation.

•Fair market value of leased asset—The fair market value of leased retail property is generally

estimated based on comparable market data or consideration received from the landlord. Fair market

value is used in determining whether the lease is accounted for as an operating lease or a capital lease.

A lease is considered a capital lease if the net present value of the lease payments is greater than 90%

of the fair market value of the property. Increasing the fair market value reduces the probability that a

lease will be considered a capital lease. Fair market value is also used in determining the amount of

property and related financing obligation to be recognized on our balance sheet for certain leased

properties which are considered owned for accounting purposes.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

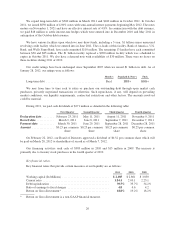

All of our long-term debt at year-end 2011 is at fixed interest rates and, therefore, is not affected by changes

in interest rates. When our long-term debt instruments mature, we may refinance them at then existing market

interest rates, which may be more or less than interest rates on the maturing debt.

Cash equivalents and long-term investments earn interest at variable rates and are affected by changes in

interest rates. During 2011, average investments were $1.6 billion and average yield was 0.3%. If interest rates

on the average 2011 variable rate cash equivalents and long-term investments increased by 100 basis points, our

annual interest income would also increase by approximately $16 million assuming comparable investment

levels.

We share in the net risk-adjusted revenue of the Kohl’s credit card portfolio as defined by the sum of

finance charges, late fees and other revenue less write-offs of uncollectible accounts. We also share the costs of

funding the outstanding receivables if interest rates were to exceed defined rates. As a result, our share of profits

from the credit card portfolio may be negatively impacted by increases in interest rates. The reduced profitability,

if any, will be impacted by various factors, including our ability to pass higher funding costs on to the credit card

holders and the outstanding receivable balance, and can not be reasonably estimated at this time.

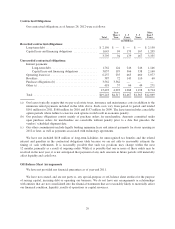

Item 8. Financial Statements and Supplementary Data

The financial statements are included in this report beginning on page F-3.

Item 9. Changes In and Disagreements with Accountants on Accounting and Financial Disclosures

None

Item 9A. Controls and Procedures

(a) Evaluation of Disclosure Controls and Procedures

Under the supervision and with the participation of our management, including our Chief Executive Officer

and Chief Financial Officer, we carried out an evaluation of the effectiveness of the design and operation of our

disclosure controls and procedures (the “Evaluation”) at a reasonable assurance level as of the last day of the

period covered by this Report.

33