Kohl's 2011 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2011 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

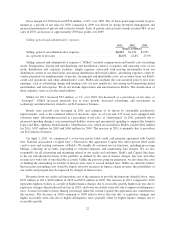

Most of our vendor allowance agreements are supported by signed contracts which are binding, but informal

in nature. The terms and conditions of these arrangements vary significantly from vendor to vendor and are

influenced by, among other things, the type of merchandise to be supported. Vendor allowances will fluctuate

based on the amount of promotional and clearance markdowns necessary to liquidate the inventory as well as

advertising and other reimbursed costs.

Insurance Reserve Estimates

We use a combination of insurance and self-insurance for a number of risks.

We retain the initial risk of $500,000 per occurrence in workers’ compensation claims and $250,000 per

occurrence in general liability claims. We record reserves for workers’ compensation and general liability claims

which include the total amounts that we expect to pay for a fully developed loss and related expenses, such as

fees paid to attorneys, experts and investigators. The fully developed loss includes amounts for both reported

claims and incurred, but not reported losses.

We use a third-party actuary to estimate the liabilities associated with these risks. The actuary considers

historical claims experience, demographic and severity factors and actuarial assumptions to estimate the

liabilities associated with these risks. As of January 28, 2012, estimated liabilities for workers’ compensation and

general liability claims, excluding administrative expenses and before pre-funding, were approximately $80

million.

A change in claims frequency and severity of claims from historical experience as well as changes in state

statutes and the mix of states in which we operate could result in a change to the required reserve levels. Changes

in actuarial assumptions could also have an impact on estimated reserves. Historically, our actuarial estimates

have not been materially different from actual results.

We are fully self-insured for employee-related health care benefits, a portion of which is paid by our

associates. We use a third-party actuary to estimate the liability for incurred, but not reported, health care claims.

This estimate uses historical claims information as well as estimated health care trends. As of January 28, 2012,

we had recorded approximately $14 million for medical, pharmacy and dental claims which were incurred in

2011 and expected to be paid in 2012. Historically, our actuarial estimates have not been materially different

from actual results.

Effective January 1, 2012, we are self-insured for a portion of our property losses. As there were no

significant property losses in January 2012, we had no related reserves as of January 28, 2012.

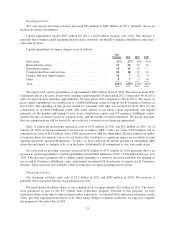

Impairment of Assets

As of January 28, 2012, our investment in buildings and improvements, before accumulated depreciation,

was $9 billion. We review these buildings and improvements for impairment when an event or changes in

circumstances, such as decisions to close a store or significant operating losses, indicate the carrying value of the

asset may not be recoverable.

For operating stores, a potential impairment has occurred if projected future undiscounted cash flows

expected to result from the use and eventual disposition of the store assets are less than the net carrying amount

of the assets. If required, we would record an impairment loss equal to the amount by which the carrying amount

of the asset exceeds its fair value. We estimate fair value as the net present value of cash flows expected to result

from the use and eventual disposition of the assets.

When determining the stream of projected future cash flows associated with an individual store,

management estimates future store performance including sales growth rates, gross margin and controllable

31