Frontier Communications 2013 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2013 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

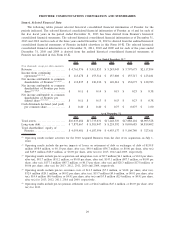

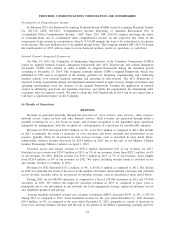

Goodwill by reporting unit (operating segment) at December 31, 2013 is as follows:

($ in thousands) 2013

Central .................................................................. $1,815,498

East..................................................................... 2,003,574

National. . . .............................................................. 1,218,113

West .................................................................... 1,300,534

Total Goodwill. ..................................................... $6,337,719

Enterprise values for rural ILEC properties are typically quoted as a multiple of cash flow or EBITDA.

Marketplace company comparisons and analyst reports support a range of fair values around a multiple of 5.5

to 7.5 times annualized EBITDA. For the purpose of the goodwill impairment test we define EBITDA as

operating income, net of acquisition and integration costs, non-cash pension and OPEB costs, pension

settlement costs, gain on sale of Mohave partnership interest and severance costs, plus depreciation and

amortization. We determined the fair value estimates using 6.25 times EBITDA but also used lower EBITDA

multiples to gauge the sensitivity of the estimate and its effect on the margin of excess of fair value over the

carrying values of the reporting units. Total fair value determined in this manner is then allocated to the

reporting units based upon each unit’s relative share of consolidated EBITDA. Our method of determining fair

value has been consistently applied for the three years ending December 31, 2013.

The Company monitors relevant circumstances, including general economic conditions, enterprise value

EBITDA multiples for other rural ILEC properties, the Company’s overall financial performance and the

market prices for the Company’s common stock, and the potential impact that changes in such circumstances

might have on the valuation of the Company’s goodwill or other intangible assets. If our goodwill or other

intangible assets are determined to be impaired in the future, we may be required to record a non-cash charge

to earnings during the period in which the impairment is determined.

Depreciation and Amortization

The calculation of depreciation and amortization expense is based upon the estimated useful lives of the

underlying property, plant and equipment and identifiable finite-lived intangible assets. Depreciation expense is

principally based on the composite group method for substantially all of our property, plant and equipment

assets. Given the varying estimated useful lives of our property, plant and equipment assets, the Company

utilizes multiple asset categories with separately determined composite lives and individual depreciation rates

for each asset category.

Within the composite group method, we group individual assets, including cable and wire, into asset

categories utilizing homogeneous characteristics, where such assets (i) are principally used in the same manner

throughout the company, (ii) are subject to similar operating conditions and (iii) have similar estimated useful

lives. Examples of the asset categories we utilize include aerial cable-copper, aerial cable-fiber, aerial cable-

station connections, underground cable-copper and underground cable-fiber. As a result of continuing changes

in technology, an independent study is conducted annually to update the estimated remaining useful lives of all

individual asset categories. The annual study includes models that consider actual usage, replacement history

and certain assumptions about technology evolution to estimate the remaining useful lives of our asset base by

asset category. The latest study was completed in the fourth quarter of 2013 and after review and analysis of

the results, we changed the remaining useful lives for certain plant assets as of October 1, 2013, with an

immaterial impact to depreciation expense. Our composite depreciation rate for plant assets was 6.24% as a

result of this study. There have been no significant changes to the ranges of estimated useful lives for the

individual asset categories, including the cable and wire asset groups, during the three years ended December

31, 2013.

Our finite-lived intangibles are customer lists acquired in the 2010 Transaction that were recorded at an

estimated fair value of $2.5 billion with an estimated useful life of nine years for the residential customer list,

and 12 years used for the business customer list. For both classes of assets, an accelerated method (the “sum of

the years digits” method) is used to amortize the intangible assets, based on the projected revenue stream of

each asset class. Our Frontier legacy customer list did not distinguish between business and residential classes.

39

FRONTIER COMMUNICATIONS CORPORATION AND SUBSIDIARIES