Costco 2009 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2009 Costco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

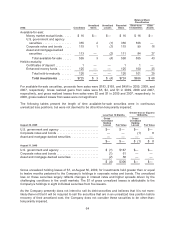

In May 2009, the FASB issued SFAS No. 165, “Subsequent Events” (SFAS 165), which establishes

general standards of accounting for and disclosure of events that occur after the balance sheet date

but before financial statements are issued or are available to be issued. SFAS 165 applies

prospectively to both interim and annual financial periods ending after June 15, 2009. The Company

adopted these new requirements in its fourth quarter of 2009. Adoption of this standard had no material

impact on the Company’s consolidated financial statements.

In April 2009, three FASB Staff Positions (FSP) were issued addressing fair value of financial

instruments: FSP FAS 157-4, “Determining Fair Value When the Volume and Level of Activity for the

Asset or Liability Have Significantly Decreased and Identifying Transactions That Are Not Orderly”

addresses determining fair values in inactive markets; FSP FAS 115-2, “Recognition and Presentation

of Other-Than-Temporary Impairments” addresses other-than-temporary impairments for debt

securities; and FSP FAS 107-1, “Disclosures about Fair Value of Financial Instruments” requires

interim disclosures about fair value of financial instruments. The Company adopted these FSPs in its

fourth quarter of 2009, with no material impact on the Company’s consolidated financial statements.

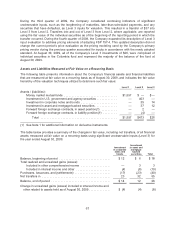

In September 2006, the FASB issued SFAS No 157, “Fair Value Measurements” (SFAS 157), which

establishes a framework for measuring fair value and requires expanded disclosures regarding fair

value measurements. In February 2008, the FASB issued FSP FAS 157-2, “Effective Date of FASB

Statement 157” (FSP 157-2), which allows for the deferral of the adoption date of SFAS 157 for all

nonfinancial assets and nonfinancial liabilities, except those that are recognized or disclosed at fair

value in the financial statements on a recurring basis. The Company elected to defer the adoption of

SFAS 157 for the assets and liabilities within the scope of FSP 157-2 until August 31, 2009, the

beginning of its fiscal year 2010. In October 2008, the FASB issued FSP FAS 157-3, “Determining the

Fair Value of a Financial Asset in a Market That Is Not Active” (FSP 157-3), which clarifies the

application of SFAS 157 when the market for a financial asset is inactive. The adoption of SFAS 157

for those assets and liabilities not subject to the deferral permitted by FSP 157-2 did not have a

material impact on the Company’s financial position or results of operations and is summarized in Note

3. The Company does not expect the adoption of SFAS 157 for non-financial assets and liabilities to

have a material impact on its consolidated financial statements.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated

Financial Statements, an Amendment of Accounting Research Bulletin No 51” (SFAS 160). SFAS 160

establishes accounting and reporting standards for ownership interests in subsidiaries held by parties

other than the parent, changes in a parent’s ownership of a noncontrolling interest, calculation and

disclosure of the consolidated net income attributable to the parent and the noncontrolling interest,

changes in a parent’s ownership interest while the parent retains its controlling financial interest and

fair value measurement of any retained noncontrolling equity investment. SFAS 160 is effective for

financial statements issued for fiscal years beginning after December 15, 2008, and interim periods

within those fiscal years. Early adoption is prohibited. The Company must adopt these new

requirements in its first quarter of fiscal 2010. SFAS 160 will change the accounting and reporting for

minority interests, and require expanded disclosure.

In December 2007, the FASB issued SFAS No. 141R, “Business Combinations” (SFAS 141R), which

establishes principles and requirements for the reporting entity in a business combination, including

recognition and measurement in the financial statements of the identifiable assets acquired, the

liabilities assumed, and any noncontrolling interest in the acquiree. SFAS 141R applies prospectively to

business combinations for which the acquisition date is on or after the beginning of the first annual

reporting period beginning on or after December 15, 2008, and interim periods within those fiscal

years. The Company must adopt these new requirements in its first quarter of fiscal 2010.

Except as noted above, the Company is in the process of evaluating the impact that adoption of these

standards will have on its future consolidated financial statements.

62