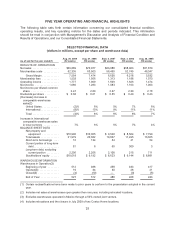

Costco 2009 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2009 Costco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

Changes in accounting standards and subjective assumptions, estimates and judgments by

management related to complex accounting matters could significantly affect our financial

results.

Generally accepted accounting principles and related accounting pronouncements, implementation

guidelines and interpretations with regard to a wide range of matters that are relevant to our business,

including, but not limited to, revenue recognition, sales returns reserves, impairment of long-lived

assets and warehouse closing costs, inventories, self-insurance, income taxes, unclaimed property

laws and litigation, are highly complex and involve many subjective assumptions, estimates and

judgments by our management. Changes in these rules or their interpretation or changes in underlying

assumptions, estimates or judgments by our management could significantly change our reported or

expected financial performance. Provisions for losses related to self-insured risks are generally based

upon independent actuarially determined estimates. The assumptions underlying the ultimate costs of

existing claim losses can be highly unpredictable, which can affect the liability recorded for such

claims. For example, variability in inflation rates of health care costs inherent in these claims can affect

the amounts realized. Similarly, changes in legal trends and interpretations, as well as a change in the

nature and method of how claims are settled can impact ultimate costs. Although our estimates of

liabilities incurred do not anticipate significant changes in historical trends for these variables, any

changes could have a considerable effect upon future claim costs and currently recorded liabilities and

could materially impact our consolidated financial statements.

Changes in Tax Rates

We compute our income tax provision based on enacted tax rates in the countries in which we operate.

As the tax rates vary among countries, a change in earnings attributable to the various jurisdictions in

which we operate could result in an unfavorable change in our overall tax provision. Additionally, any

change in the enacted tax rates, any adverse outcome in connection with any income tax audits in any

jurisdiction, or any change in the pronouncements relating to accounting for income taxes may have a

material adverse affect on our financial condition, results of operation, or cash flows.

Failure of our internal control over financial reporting could limit our ability to report our

financial results accurately and timely.

Our management is responsible for establishing and maintaining adequate internal control over

financial reporting. Internal control over financial reporting is designed to provide reasonable assurance

regarding the reliability of financial reporting for external purposes in accordance with U.S. generally

accepted accounting principles. Internal control over financial reporting includes: maintaining records

that in reasonable detail accurately and fairly reflect our transactions; providing reasonable assurance

that transactions are recorded as necessary for preparation of the financial statements; providing

reasonable assurance that our receipts and expenditures of our assets are made in accordance with

management authorization; and providing reasonable assurance that unauthorized acquisition, use or

disposition of our assets that could have a material effect on the financial statements would be

prevented or detected on a timely basis. Because of its inherent limitations, internal control over

financial reporting is not intended to and cannot provide absolute assurance that a misstatement of our

financial statements would be prevented or detected. Any failure to maintain an effective system of

internal control over financial reporting could limit our ability to report our financial results accurately

and timely or to detect and prevent fraud.

18