Capital One 1998 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 1998 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60

|

|

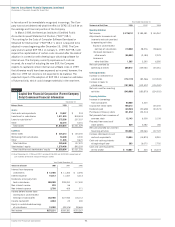

51 Capital One Financial Corporation

During 1996, the Bank received regulatory approval and estab-

lished a branch office in the United Kingdom. In connection with

such approval, the Company committed to the Federal Reserve

that, for so long as the Bank maintains a branch in the United

Kingdom, the Company will maintain a minimum Tier 1 Leverage

ratio of 3.0%. As of December 31, 1998 and 1997, the Company’s

Tier 1 Leverage ratio was 13.49% and 13.83%, respectively.

Additionally, certain regulatory restrictions exist which limit the

ability of the Bank and the Savings Bank to transfer funds to the

Corporation. As of December 31, 1998, retained earnings of the

Bank and the Savings Bank of $117,191 and $16,189, respec-

tively, were available for payment of dividends to the Corporation

without prior approval by the regulators. The Savings Bank, how-

ever, is required to give the OTS at least thirty days advance notice

of any proposed dividend and the OTS, in its discretion, may object

to such dividend.

Note L

Commitments and Contingencies

As of December 31, 1998, the Company had outstanding lines of

credit of approximately $49,200,000 committed to its customers.

Of that total commitment, approximately $31,800,000 was

unused. While this amount represented the total available lines of

credit to customers, the Company has not experienced, and does

not anticipate, that all of its customers will exercise their entire

available line at any given point in time. The Company generally

has the right to increase, reduce, cancel, alter or amend the terms

of these available lines of credit at any time.

Certain premises and equipment are leased under agreements

that expire at various dates through 2008, without taking into con-

sideration available renewal options. Many of these leases provide

for payment by the lessee of property taxes, insurance premiums,

cost of maintenance and other costs. In some cases, rentals are

subject to increase in relation to a cost of living index. Total rental

expense amounted to $18,242, $13,644 and $12,603 for the

years ended December 31, 1998, 1997 and 1996, respectively.

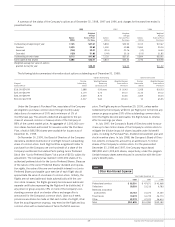

Future minimum rental commitments as of December 31,

1998, for all non-cancelable operating leases with initial or remain-

ing terms of one year or more are as follows:

1999 $ 19,097

2000 17,943

2001 16,687

2002 15,884

2003 14,934

Thereafter 24,980

Total $109,525

In connection with the transfer of substantially all of Signet

Bank’s credit card business to the Bank in November 1994,

the Company and the Bank agreed to indemnify Signet Bank

(which was acquired by First Union on November 30, 1997) for

Note K

Regulatory Matters

The Bank and the Savings Bank are subject to capital adequacy

guidelines adopted by the Federal Reserve Board (the “Federal

Reserve”) and the Office of Thrift Supervision (the “OTS”) (collec-

tively, the “regulators”), respectively. The capital adequacy guide-

lines and the regulatory framework for prompt corrective action

require the Bank and the Savings Bank to maintain specific capital

levels based upon quantitative measures of their assets, liabilities

and off-balance sheet items. The inability to meet and maintain

minimum capital adequacy levels could result in the regulators tak-

ing actions that could have a material effect on the Company’s con-

solidated financial statements. Additionally, the regulators have

broad discretion in applying higher capital requirements. Regula-

tors consider a range of factors in determining capital adequacy,

such as an institution’s size, quality and stability of earnings, inter-

est rate risk exposure, risk diversification, management expertise,

asset quality, liquidity and internal controls.

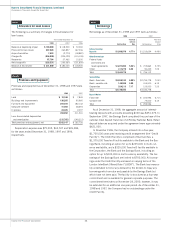

The most recent notifications received from the regulators cate-

gorized the Bank and the Savings Bank as “well-capitalized.” To be

categorized as “well-capitalized,” the Bank and the Savings Bank

must maintain minimum capital ratios as set forth in the table

below. As of December 31, 1998, there were no conditions or

events since the notifications discussed above that management

believes would have changed either the Bank or the Savings Bank’s

capital category.

Minimum for To Be “Well-

Capital Capitalized” Under

Adequacy Prompt Corrective

Ratios Purposes Action Provisions

December 31, 1998

Capital One Bank

Tier 1 Capital 11.38% 4.00% 6.00%

Total Capital 13.88 8.00 10.00

Tier 1 Leverage 10.24 4.00 5.00

Capital One, F.S.B.(1)

Tangible Capital 9.46% 1.50% 6.00%

Total Capital 13.87 12.00 10.00

Core Capital 9.46 8.00 5.00

December 31, 1997

Capital One Bank

Tier 1 Capital 10.49% 4.00% 6.00%

Total Capital 13.26 8.00 10.00

Tier 1 Leverage 10.75 4.00 5.00

Capital One, F.S.B.(1)

Tangible Capital 11.26% 1.50% 6.00%

Total Capital 17.91 12.00 10.00

Core Capital 11.26 8.00 5.00

(1) Until June 30, 1999, the Savings Bank is subject to capital requirements that exceed

minimum capital adequacy requirements, including the requirement to maintain

a minimum Core Capital ratio of 8% and a Total Capital ratio of 12%.