Capital One 1998 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 1998 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

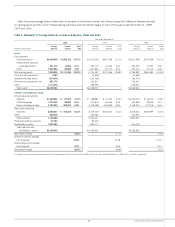

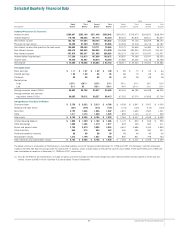

Table 12: Interest Rate Sensitivity

As of December 31, 1998, Subject to Repricing

Within >180 Days- >1 Year- Over

(Dollars in Millions) 180 Days 1 Year 5 Years 5 Years

Earning assets:

Federal funds sold and resale agreements $(262

Interest-bearing deposits at other banks 22

Securities available for sale 148 $ (95 $(1,082 $ (472

Consumer loans 3,111 161 2,885

Total earning assets 3,543 256 3,967 472

Interest-bearing liabilities:

Deposits 1,019 243 738

Other borrowings 1,644

Senior and deposit notes 467 470 2,123 679

Total interest-bearing liabilities 3,130 713 2,861 679

Non-rate related net assets (855)

Interest sensitivity gap 413 (457) 1,106 (1,062)

Impact of swaps 3,264 (138) (2,119) (1,007)

Impact of consumer loan securitizations (3,847) (493) 4,966 (626)

Interest sensitivity gap adjusted for impact of securitizations and swaps $ (170) $(1,088) $(3,953 $(2,695)

Adjusted gap as a percentage of managed assets (.82)% (5.28)% 19.17% (13.07)%

Adjusted cumulative gap $ (170) $(1,258) $(2,695

Adjusted cumulative gap as a percentage of managed assets (.82)% (6.10)% 13.07% 0.00)%

31 Capital One Financial Corporation

Product and Market Opportunities

The Company’s strategy for future growth has been, and is expected

to continue to be, to apply its proprietary IBS to its lending

business as well as to other businesses, both financial and non-

financial, including telecommunications services. The Company

will seek to identify new product opportunities and to make

informed investment decisions regarding new and existing prod-

ucts. The Company’s lending and other financial and non-financial

products are subject to competitive pressures, which management

anticipates will increase as these markets mature.

Lending Lending includes credit card and other consumer lending

products. Credit card opportunities include, and are expected to

continue to include, low introductory and intermediate rate balance

transfer products, low non-introductory rate products, as well as

other customized credit card products, such as secured cards,

affinity and co-branded cards, student cards and other cards

tailored for specific consumer segments. The Company expects

continued growth across a broad spectrum of new and existing

customized products, which are distinguished by a varied range of

credit lines, pricing structures and other characteristics. For exam-

ple, the Company’s low non-introductory rate products, which are

marketed to consumers with the best established credit profiles,

are characterized by higher credit lines, lower yields and an expec-

tation of lower delinquencies and credit losses than the traditional

low introductory rate balance transfer products. On the other hand,

certain other customized card products are characterized by lower

credit lines, higher yields (including fees) and in some cases,

Business Outlook

Earnings, Goals and Strategies

This business outlook section summarizes the Company’s expecta-

tions for earnings for the year ending December 31, 1999, and its

primary goals and strategies for continued growth. The statements

contained in this section are based on management’s current

expectations. Certain statements are forward looking and, there-

fore, actual results could differ materially. Factors which could

materially influence results are set forth throughout this section

and in the Company’s Annual Report on Form 10-K for the

year ended December 31, 1998 (Part I, Item 1, Risk Factors).

The Company has set an earnings target increase of approxi-

mately 30% over 1998 earnings and a return on equity in excess of

20%. As discussed elsewhere in this report and below, the Com-

pany’s actual earnings are a function of its revenues (net interest

income and non-interest income on its earning assets), consumer

usage and payment patterns, credit quality of its earning assets

(which affects fees and charge-offs), marketing expenses and

operating expenses.

Table 12 reflects the interest rate repricing schedule for earning assets and interest-bearing liabilities as of December 31, 1998.