Capital One 1998 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 1998 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

21 Capital One Financial Corporation

During 1997, the Company modified its methodology for charg-

ing off credit card loans (net of any collateral) to 180 days past-

due, from the prior practice of charging off loans during the next

billing cycle after becoming 180 days past-due. As a result, 1997

managed net interest income was reduced by $15.1 million and

managed non-interest income was reduced by $8.0 million for the

reversal of previously accrued finance charges and fee income. In

addition, this modification increased managed net charge-offs by

$47.4 million in 1997. Also, during 1997, the Company began

recognizing the estimated uncollectible portion of finance charge

and fee income receivables, which decreased loans by $50.2 mil-

lion, managed net interest income by $19.8 million and managed

non-interest income by $30.4 million. Risk adjusted revenue and

risk adjusted margin, without these modifications, would have been

$1.3 billion and 8.92%, respectively, in 1997.

Table 3 provides income statement data and ratios for the

Company’s managed consumer loan portfolio. The causes of

increases and decreases in the various components of risk adjusted

revenue are discussed in further detail in subsequent sections of

this analysis.

tors have continuously solicited the Company’s customers with sim-

ilar interest rate strategies. Management believes the competition

has put, and will continue to put, additional pressure on the

Company’s pricing strategies.

By applying its IBS and in response to dynamic competitive

pressures, the Company also targets a significant amount of its

marketing expense to other credit card product opportunities.

Examples of such products include secured cards and other cus-

tomized card products including affinity and co-branded cards, stu-

dent cards and other cards targeted to certain markets that are

underserved by the Company’s competitors. These products do not

have the immediate impact on managed loan balances of the bal-

ance transfer products but typically consist of lower credit limit

accounts and balances that build over time. The terms of these

customized card products tend to include annual membership fees

and higher annual finance charge rates. The profile of the con-

sumers targeted for these products, in some cases, may also tend

to result in higher account delinquency rates and consequently

higher past-due and overlimit fees as a percentage of loan receiv-

ables outstanding than the balance transfer products.

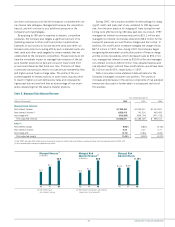

Table 3: Managed Risk Adjusted Revenue

Year Ended December 31

(Dollars in Thousands) 1998 1997 1996

Managed Income Statement:

Net interest income $1,700,424 $1,299,317 $1,013,557

Non-interest income(1) 1,066,413 743,516 460,492

Net charge-offs (810,306) (856,704) (477,732)

Risk adjusted revenue $1,956,531 $1,186,129 $ 996,317

Ratios(2):

Net interest margin 9.95% 8.86% 8.16%

Non-interest income 6.24 5.07 3.71

Net charge-offs (4.74) (5.84) (3.85)

Risk adjusted margin 11.45% 8.09% 8.02%

(1) For 1997, excludes $32 million pre-tax incremental impact on credit card securitizations income resulting from the implementation of SFAS 125.

(2) As a percentage of average managed earning assets.

$2.8

$2.1

$1.5

Managed Revenue(1)

(In Billions)

96 97 98

$2.0

$1.2

$1.0

Managed Risk

Adjusted Revenue(2)

(In Billions)

96 97 98

(1) Net interest and

non-interest income.

(2) Net interest income plus non-interest

income less net charge-offs.

11.45%

8.09%

8.02%

Managed Risk

Adjusted Margin

96 97 98