Capital One 1998 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 1998 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

22Capital One Financial Corporation

Management’s Discussion and Analysis of Financial Condition and Results of Operations (continued)

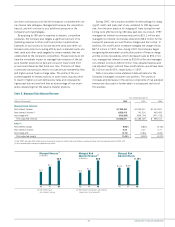

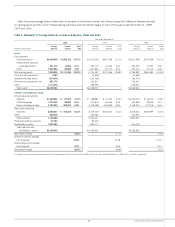

Reported net interest income for the year ended December 31,

1997 was $383.1 million, compared to $365.5 million for 1996,

representing an increase of $17.6 million, or 5%. Average earning

assets increased 20% to $5.8 billion for the year ended December

31, 1997, from $4.8 billion in 1996. The reported net interest

margin decreased to 6.66% in 1997, from 7.62% in 1996 and

was primarily attributable to a 110 basis point decrease in the yield

on consumer loans to 15.11% for the year ended December 31,

1997, from 16.21% for 1996. The yield on consumer loans

decreased due to the removal from the balance sheet through secu-

ritization of higher yielding credit card products during the fourth

quarter of 1996 and a $24.4 million reduction in reported con-

sumer loan income as a result of modifications in the charge-off

policy and finance charge and fee income recognition previously

discussed. These decreases were offset by an increase in the

amount of past-due fees charged from both a change in terms and

an increase in the delinquency rate as compared to 1996.

The managed net interest margin for the year ended December

31, 1997, increased to 8.86% from 8.16% for the year ended

December 31, 1996. This increase was primarily the result of a 97

basis point increase in consumer loan yield for the year ended

December 31, 1997, offset by an 11 basis point increase in bor-

rowing costs for the same period, as compared to 1996. The

increase in consumer loan yield to 15.73% for the year ended

December 31, 1997, from 14.76% in 1996 principally reflected

the 1997 repricing of introductory rate loans, changes in product

mix and the increase in past-due fees charged on delinquent

accounts noted above. The average rate paid on borrowed funds

increased slightly to 5.95% for the year ended December 31,

1997, from 5.84% in 1996, primarily reflecting a relatively steady

short-term interest rate environment during 1997 and 1996.

Net Interest Income

Net interest income is interest and past-due fees earned from the

Company’s consumer loans and securities less interest expense on

borrowings, which include interest-bearing deposits, other borrow-

ings and borrowings from senior and deposit notes.

Reported net interest income for the year ended December 31,

1998, was $694.8 million compared to $383.1 million for 1997,

representing an increase of $311.6 million, or 81%. Net interest

income increased as a result of growth in earning assets and an

increase in the net interest margin. Average earning assets

increased 26% for the year ended December 31, 1998, to $7.2

billion from $5.8 billion for the year ended December 31, 1997.

The reported net interest margin increased to 9.62% in 1998, from

6.66% in 1997 primarily attributable to a 364 basis point increase

in the yield on consumer loans to 18.75% for the year ended

December 31, 1998, from 15.11% for the year ended December

31, 1997. The yield on consumer loans increased primarily due to

an increase in the amount and frequency of past-due fees as com-

pared to the prior year. In addition, the Company’s continued shift

to higher yielding products, offset by growth in low non-introductory

rate products, contributed to the increase in yield on consumer

loans during the same periods.

The managed net interest margin for the year ended December

31, 1998, increased to 9.95% from 8.86% for the year ended

December 31, 1997. This increase was primarily the result of a

126 basis point increase in consumer loan yield for the year ended

December 31, 1998, offset by an increase of nine basis points in

borrowing costs for the same period, as compared to 1997. The

increase in consumer loan yield to 16.99% for the year ended

December 31, 1998, from 15.73% in 1997 principally reflected

increases in the amount and frequency of changes in past-due fees

and growth in higher yielding loans. The average rate paid on bor-

rowed funds increased slightly to 6.04% for the year ended Decem-

ber 31, 1998, from 5.95% in 1997, reflecting the Company’s shift

to more fixed rate funding to match the increase in fixed rate con-

sumer loan products.