Capital One 1998 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 1998 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

|

|

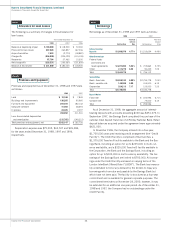

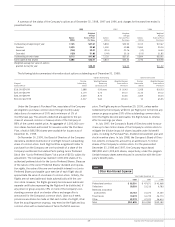

43 Capital One Financial Corporation

liabilities or off-balance sheet items. The Company enters into for-

ward foreign currency exchange contracts (“f/x contracts”) and cur-

rency swaps to reduce its sensitivity to changing foreign currency

exchange rates. All of the Company’s f/x contracts and currency

swaps are designated and effective as hedges of specific assets or

liabilities. The Company does not hold or issue derivative financial

instruments for trading purposes.

Swap agreements involve the periodic exchange of payments

over the life of the agreements. Amounts paid or received on inter-

est rate and currency swaps are recorded on an accrual basis as an

adjustment to the related income or expense of the item to which

the agreements are designated. As of December 31, 1998, the

related amount payable to counterparties was $2,463. As of

December 31, 1997, the related amount receivable from counter-

parties was $2,771. Changes in the fair value of interest rate swaps

are not reflected in the accompanying financial statements, where

designated to existing or anticipated assets, liabilities or off-bal-

ance sheet items and where swaps effectively modify or reduce

interest rate sensitivity.

F/x contracts represent an agreement to exchange a specified

notional amount of two different currencies at a specified exchange

rate on a specified future date. Changes in the fair value of f/x con-

tracts and currency swaps are recorded in the period in which they

occur as foreign currency gains or losses in other non-interest

income, effectively offsetting the related gains or losses on the

items to which they are designated.

Realized and unrealized gains or losses at the time of maturity,

termination, sale or repayment of a derivative contract are recorded

in a manner consistent with its original designation. Amounts are

deferred and amortized as an adjustment to the related income or

expense over the original period of exposure, provided the desig-

nated asset, liability or off-balance sheet item continues to exist, or

in the case of anticipated transactions, is probable of occurring.

Realized and unrealized changes in the fair value of swaps or f/x

contracts, designated with items that no longer exist or are no

longer probable of occurring, are recorded as a component of the

gain or loss arising from the disposition of the designated item.

Interest rate and foreign currency exchange rate risk manage-

ment contracts are generally expressed in notional principal or

contract amounts that are much larger than the amounts potentially

at risk for nonperformance by counterparties. In the event of non-

performance by the counterparties, the Company’s credit exposure

on derivative financial instruments is limited to the value of the

contracts that have become favorable to the Company. The

Company actively monitors the credit ratings of its counterparties.

Under the terms of certain swaps, each party may be required

to pledge collateral if the market value of the swaps exceeds an

amount set forth in the agreement or in the event of a change in its

credit rating.

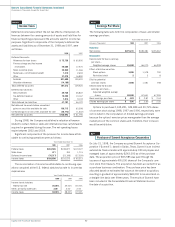

Securitizations

The Company records gains or losses on the securitization of con-

sumer loan receivables on the date of sale based on the estimated

fair value of assets sold and retained and liabilities incurred in the

sale. Gains represent the present value of estimated cash flows the

Company has retained over the estimated outstanding period of the

receivables. This excess cash flow essentially represents an “inter-

est only”(“I/O”) strip, consisting of the excess of finance charges

and past-due fees over the sum of the return paid to certificatehold-

ers, estimated contractual servicing fees and credit losses. The I/O

strip is carried at fair value, with changes in the fair value reported

as a component of cumulative other comprehensive income. Cer-

tain estimates inherent in the determination of the fair value of

the I/O strip are influenced by factors outside the Company’s

control, and as a result, such estimates could materially change

in the near term. The gains on securitizations and other income

from securitizations are included in servicing and securitizations

income.

In June 1996, the Financial Accounting Standards Board

(“FASB”) issued Statement of Financial Accounting Standards

(“SFAS”) No. 125, “Accounting for Transfers and Servicing of

Financial Assets and Extinguishments of Liabilities”(“SFAS 125”),

which was effective January 1, 1997. The Company prospectively

adopted the requirements of SFAS 125 for the securitization of

consumer loans. The incremental effect of applying the new

requirements was to increase servicing and securitizations income

in 1997 by $32,000 ($19,840, net of tax). Prior to 1997, no gains

were recorded due to the relatively short average life of the con-

sumer loans securitized. Excess servicing fee income was recorded

over the life of each sale transaction.

Off-Balance Sheet Financial Instruments

The nature and composition of the Company’s assets and liabilities

and off-balance sheet items expose the Company to interest rate

risk. The Company’s foreign currency denominated assets and lia-

bilities expose it to foreign currency exchange rate risk. To mitigate

these risks, the Company uses certain types of derivative financial

instruments. The Company enters into interest rate swap agree-

ments (“interest rate swaps”) in the management of its interest rate

exposure. All of the Company’s interest rate swaps are designated

and effective as hedges of specific existing or anticipated assets,