CVS 2012 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2012 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

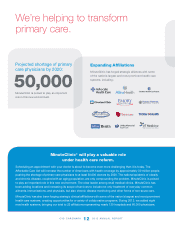

We’ve grown our PBM book of business by approxi-

mately 50 percent since 2010, delivering $24 billion of

net new business over this period. In the 2013 selling

season, we retained 96 percent of our book of business.

We also won well over $4 billion in gross new business

and approximately $400 million in net new business.

It’s worth noting that these gains came across customer

segments, including employers, commercial health

plans, Medicare Part D, and Medicaid.

Medicare has quickly emerged as a major payor for

prescription drugs in the United States, and our PBM

is currently a strong number three player in the Part D

market with roughly 6.5 million lives. This includes the

lives we serve through our SilverScript prescription

drug plans, as well as other lives where we serve as the

PBM for health plan clients. With baby boomers turning

65 at the rate of 10,000 people per day, along with their

growing utilization of prescription medications, we see

the Medicare market as an attractive growth area.

Managed Medicaid represents another critical growth

segment for us, as health care reform could add up

to 15 million new lives to Medicaid rolls in the coming

years. We are currently the clear leader in the Managed

Medicaid PBM market with an estimated 31 percent

share. We have continued to win new clients and have

also seen existing clients expand membership as states

move from a fee-for-service model. Our success is due

in part to our ability to tailor our programs and opera-

tions to support the unique needs of this segment.

Our specialty pharmacy business continues to grow

rapidly, with enterprise-wide specialty revenues of

more than $18 billion in 2012. The specialty market is

expected to grow to approximately $120 billion in 2016,

roughly double the size of the market in 2010. That

means that by late 2016, it could account for roughly

one-third of total pharmacy spend in the United States.

This rapid increase in specialty drug costs presents

challenges for our clients, so we have expanded our

capabilities to manage specialty trend across the entire

continuum of pharmacy and medical benefits. When

implementing our programs, which include Specialty

Guideline Management, exclusive pharmacy networks,

and site of care management, clients can save up to

12 to 16 percent on their specialty spend.

There is plenty of other good news coming out of our

PBM, from our collaboration with Aetna to our streamlin-

ing initiative. The latter, which involves rationalizing our

mail order pharmacies, streamlining operations, and

consolidating our claims adjudication systems, is on

track to deliver $1 billion in cumulative cost savings over

the five-year period ending in 2015.

CVS/pharmacy® gained share and outperformed

competitors on key metrics

Our retail business continued to fire on all cylinders in

2012, and we gained market share in both the pharmacy

and the front of the store. In fact, our retail share of the

prescription drug market has grown two percentage

points in the past two years to reach more than 21 percent.

We also far outpaced our peer group with 9.1 percent

growth in prescriptions dispensed. Even factoring out

the prescriptions gained during the Express Scripts-

Walgreens impasse, our underlying pharmacy growth

led the industry.

Our focus on excellence in patient care is a key driver

of our strong performance in the pharmacy. As part

of our patient care initiatives, our pharmacy teams

performed 72 million customer interventions in 2012.

Interventions like these keep our adherence rates well

above all other pharmacy retailers, helping our patients

stay healthy and driving savings for payors.

Another way in which we can control health care costs

is by moving patients to lower-cost, generic drug alterna-

tives when available and clinically appropriate. Given

that generics produce greater profits for us than branded

drugs, we can improve profitability even as we lower

costs for patients and payors. The opportunity for us

in this area remains significant for the next few years.

“ We’ve grown our PBM book of business by approximately

50 percent since 2010, delivering $24 billion of net new

business over this period.”

CVS CAREMARK 2012 ANNUAL REPORT

3