CVS 2009 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2009 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

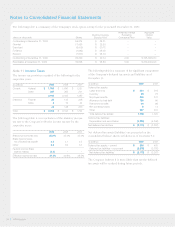

Note 6 Leases

The Company leases most of its retail and mail locations, 11

of its distribution centers and certain corporate offices under

noncancellable operating leases, with initial terms of 15 to

25 years and with options that permit renewals for additional

periods. The Company also leases certain equipment and other

assets under noncancellable operating leases, with initial terms

of 3 to 10 years. Minimum rent is expensed on a straight-line

basis over the term of the lease. In addition to minimum rental

payments, certain leases require additional payments based on

sales volume, as well as reimbursement for real estate taxes,

common area maintenance and insurance, which are expensed

when incurred.

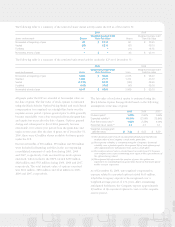

The following table is a summary of the Company’s net rental

expense for operating leases for the respective years:

in millions 2009 2008 2007

Minimum rentals $ 1,857 $ 1,691 $ 1,557

Contingent rentals 61 58 65

1,918 1,749 1,622

Less: sublease income (19) (25) (21)

$ 1,899 $ 1,724 $ 1,601

The following table is a summary of the future minimum lease

payments under capital and operating leases as of Decem-

ber 31, 2009:

Capital Operating

in millions Leases Leases

2010 $ 17 $ 2,094

2011 17 1,877

2012 18 1,953

2013 18 1,855

2014 18 1,657

Thereafter 236 17,477

Total future lease payments $ 324 $ 26,913

Less: imputed interest (170)

Present value of capital lease obligations $ 154

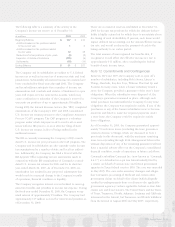

The Company finances a portion of its store development

program through sale-leaseback transactions. The properties

are sold at fair value, which approximates net book value, and

the resulting leases qualify and are accounted for as operating

leases. The operating leases that resulted from these transac-

tions are included in the above table. The Company does not

have any retained or contingent interests in the stores and does

not provide any guarantees, other than a guarantee of lease

payments, in connection with the sale-leaseback transactions.

Proceeds from sale-leaseback transactions totaled $1.6 billion

in 2009. This compares to $204 million in 2008 and $601 million

in 2007.

On July 1, 2009, the Company issued a $300 million unsecured

floating rate senior note due January 30, 2011 (the “the 2009

Floating Rate Note”). The 2009 Floating Rate Note pays interest

quarterly. The net proceeds from the 2009 Floating Rate Note

were used for general corporate purposes.

On September 8, 2009, the Company issued $1.5 billion of

6.125% unsecured senior notes due September 15, 2039 (the

“September 2009 Notes”). The September 2009 Notes pay

interest semi-annually and may be redeemed, in whole or in

part, at a defined redemption price plus accrued interest. The

net proceeds were used to repay a portion of the Company’s

outstanding commercial paper borrowings, $650 million of

unsecured senior notes and for general corporate purposes.

On September 10, 2008, the Company issued $350 million of

floating rate senior notes due September 10, 2010 (the “2008

Notes”). The 2008 Notes pay interest quarterly and may be

redeemed at any time, in whole or in part at a defined redemp-

tion price plus accrued interest. The net proceeds from the 2008

Notes were used to fund a portion of the Longs Acquisition.

On May 22, 2007, the Company issued $1.75 billion of floating

rate senior notes due June 1, 2010, $1.75 billion of 5.75%

unsecured senior notes due June 1, 2017, and $1.0 billion of

6.25% unsecured senior notes due June 1, 2027 (collectively

the “2007 Notes”). Also on May 22, 2007, the Company entered

into an underwriting agreement pursuant to which the Com-

pany agreed to issue and sell $1.0 billion of Enhanced Capital

Advantaged Preferred Securities (“ECAPS”) due June 1, 2062

to the underwriters. The ECAPS bear interest at 6.30% per year

until June 1, 2012 at which time they will pay interest based

on a floating rate. The 2007 Notes and ECAPS pay interest

semi-annually and may be redeemed at any time, in whole

or in part at a defined redemption price plus accrued interest.

The net proceeds from the 2007 Notes and ECAPS were used

to repay a portion of the bridge credit facility and commercial

paper borrowings used to fund a portion of the Longs Acquisi-

tion purchase price and retire $353 million of debt assumed as

part of the Longs Acquisition.

The credit facilities, back-up credit facilities, unsecured senior

notes and ECAPS contain customary restrictive financial and

operating covenants. The covenants do not materially affect

the Company’s financial or operating flexibility.

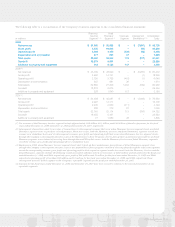

The aggregate maturities of long-term debt for each of the

five years subsequent to December 31, 2009 are $2.1 billion in

2010, $1.1 billion in 2011, $1.0 billion in 2012, $5 million in

2013 and $555 million in 2014.

2009 Annual Report 59