CVS 2009 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2009 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

the principles and requirements for how an acquirer recog-

nizes and measures in its financial statements the identifiable

assets acquired, the liabilities assumed, any noncontrolling

interest in the acquiree and the goodwill acquired. The

guidance also establishes disclosure requirements that will

enable users to evaluate the nature and financial effects of

business combinations. ASC 805 requires that income tax

benefits related to business combinations that are not recorded

at the date of acquisition are recorded as an income tax benefit

in the statement of operations when subsequently recognized.

Previously, unrecognized income tax benefits related to

business combinations were recorded as an adjustment to the

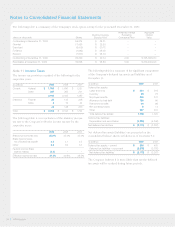

purchase price allocation when recognized. During 2009, the

Company recognized approximately $147 million of previously

unrecognized income tax benefits related to business combina-

tions (after considering the federal benefit of state taxes), plus

interest, due to the expiration of various statutes of limitations

and settlements with tax authorities. As of December 31, 2009,

the Company had approximately $20 million of unrecognized

tax benefits (after considering the federal benefit of state taxes),

plus interest, related to business combinations that would have

been treated as an adjustment to the purchase price allocation if

they would have been recognized under the previous business

combination guidance.

In April 2009, the FASB issued further guidance as it relates

to ASC 805 (formerly FASB Staff Position No. FAS 141(R)-1,

“Accounting for Assets Acquired and Liabilities Assumed in

a Business Combination That Arise from Contingencies”) to

address the initial recognition, measurement and subsequent

accounting for assets and liabilities arising from contingencies

in a business combination, and requires that such assets

acquired or liabilities assumed be initially recognized at fair

value at the acquisition date if fair value can be determined

during the measurement period. If the acquisition-date fair value

cannot be determined, the asset acquired or liability assumed

arising from a contingency is recognized only if certain criteria

are met. This guidance also requires that a systematic and

rational basis for subsequently measuring and accounting

for the assets or liabilities be developed depending on their

nature. The adoption of this guidance may have an impact

on the accounting for future business combinations, but the

effect is dependant upon acquisitions at that time.

During the first quarter of 2009, the Company adopted

SFAS No. 160, “Noncontrolling Interests in Consolidated

Financial Statements,” which is now included in ASC 810

Consolidations. This statement requires the presentation of

net income (loss) allocable to noncontrolling interests along

with net income (loss) attributable to shareholders of the

the dividends it received to service its debt, the Company had

to increase its contribution to the ESOP Trust to compensate it

for the lower dividends. This additional contribution reduced

the Company’s net earnings, which in turn, reduced the amounts

that would be accrued under the Company’s incentive compen-

sation plans.

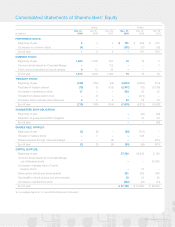

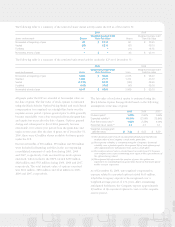

Diluted earnings per common share is computed by dividing:

(i) net earnings, after accounting for the difference between

the dividends on the ESOP preference stock and common

stock and after making adjustments for the incentive compen-

sation plans, by (ii) Basic Shares plus the additional shares

that would be issued assuming that all dilutive stock awards

are exercised and the ESOP preference stock is converted into

common stock. Options to purchase 37.7 million, 20.9 million

and 10.7 million shares of common stock were outstanding as

of December 31, 2009, December 31, 2008 and December 29,

2007, respectively, but were not included in the calculation of

diluted earnings per share because the options’ exercise prices

were greater than the average market price of the common

shares and, therefore, the effect would be antidilutive. See

Note 8 for additional information about the ESOP.

RECENTLY ADOPTED ACCOUNTING PRONOUNCEMENTS

In the third quarter of 2009, the Company adopted the

Financial Accounting Standards Board (“FASB”) Accounting

Standards Codification (“ASC”) as the source of authoritative

generally accepted accounting principles (“GAAP”) for

nongovernmental entities. The ASC does not change GAAP

but rather takes the numerous individual pronouncements

that previously constituted GAAP and reorganizes them into

approximately 90 accounting topics, and displays all topics

using a consistent structure. Citing particular content in the

ASC involves specifying the unique numeric path to the

content. The adoption of ASC did not have any effect on

the Company’s consolidated results of operations, financial

position or cash flows.

During the second quarter of 2009, the Company adopted

ASC 855 Subsequent Events (formerly Statement of Financial

Accounting Standards (“SFAS”) No. 165, “Subsequent Events”)

which establishes general standards of accounting for and

disclosure of events that occur after the balance sheet date but

prior to the issuance of the financial statements. The adoption

of this standard did not have a material impact on the Com-

pany’s consolidated results of operations, financial position,

cash flows or disclosures.

During the first quarter of 2009, the Company adopted

ASC 805 Business Combinations (“ASC 805”) (formerly SFAS

No. 141 (R), “Business Combinations”). ASC 805 establishes

2009 Annual Report 55