CVS 2009 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2009 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

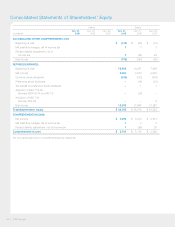

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

Cautionary Statement Concerning

Forward-Looking Statements

The Private Securities Litigation Reform Act of 1995 (the

“Reform Act”) provides a safe harbor for forward-looking

statements made by or on behalf of CVS Caremark Corpora-

tion. The Company and its representatives may, from time

to time, make written or verbal forward-looking statements,

including statements contained in the Company’s filings with

the Securities and Exchange Commission and in its reports to

stockholders. Generally, the inclusion of the words “believe,”

“expect,” “intend,” “estimate,” “project,” “anticipate,” “will,”

“should” and similar expressions identify statements that

constitute forward-looking statements. All statements address-

ing operating performance of CVS Caremark Corporation or

any subsidiary, events or developments that the Company

expects or anticipates will occur in the future, including

statements relating to revenue growth, earnings or earnings

per common share growth, free cash flow, debt ratings,

inventory levels, inventory turn and loss rates, store develop-

ment, relocations and new market entries, as well as statements

expressing optimism or pessimism about future operating

results or events, are forward-looking statements within the

meaning of the Reform Act.

The forward-looking statements are and will be based upon

management’s then-current views and assumptions regarding

future events and operating performance, and are applicable

only as of the dates of such statements. The Company

undertakes no obligation to update or revise any forward-

looking statements, whether as a result of new information,

future events, or otherwise.

By their nature, all forward-looking statements involve risks

and uncertainties. Actual results may differ materially from

those contemplated by the forward-looking statements for a

number of reasons, including, but not limited to:

• Our business is affected by the economy in general including

changes in consumer purchasing power, preferences and/or

spending patterns. These changes could affect drug utiliza-

tions trends, the number of covered lives and the financial

health of our PBM clients. Further, interest rate fluctuations

and changes in capital market conditions may affect our

ability to obtain necessary financing on acceptable terms,

our ability to secure suitable store locations under accept-

able terms and our ability to execute future sale-leaseback

transactions under acceptable terms;

Collateral Assignment Split-Dollar Life Insurance Agreements”).

The application of this guidance requires a company to

recognize a liability for the discounted value of the future

premium benefits that a company will incur through the death

of the underlying insured and provides guidance for determin-

ing a liability for the postretirement benefit obligation as well

as recognition and measurement of the associated asset on

the basis of the terms of the collateral assignment agreement.

The adoption of the content within ASC 715-60 did not have

a material impact on our consolidated results of operations,

financial position or cash flows.

Recent Accounting Pronouncement Not

Yet Effective

In June 2009, the FASB issued SFAS No. 167 (not yet codified

in ASC), “Amendments to FASB Interpretation No. 46(R),”

(“SFAS 167”). The standard amends the content within ASC 810

Consolidations (formerly FASB Interpretations (“FIN”) No. 46(R))

to require a company to analyze whether its interest in a variable

interest entity (“VIE”) gives it a controlling financial interest.

The determination of whether a company is required to

consolidate another entity is based on, among other things,

the other entity’s purpose and design and a company’s ability

to direct the activities of the other entity that most significantly

impact the other entity’s economic performance. Additional

disclosures are required to identify a company’s involvement

with the VIE and any significant changes in risk exposure due

to such involvement. SFAS 167 is effective for all new and

existing VIEs as of the beginning of the first fiscal year that

begins after November 15, 2009. We do not believe the adoption

of SFAS 167 will have a material impact on our consolidated

results of operations, financial position or cash flows.

CVS Caremark

40