CVS 2009 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2009 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

Amounts assigned to identifiable intangible assets, and their

related useful lives, are derived from established valuation

techniques and management estimates. Goodwill represents

the excess of amounts paid for acquisitions over the fair

market value of the net identifiable assets acquired.

We evaluate the recoverability of certain long-lived assets,

including intangible assets with finite lives, but excluding

goodwill and intangible assets with indefinite lives, which are

tested for impairment using separate tests, whenever events

or changes in circumstances indicate that the carrying value of

an asset may not be recoverable. We group and evaluate these

long-lived assets for impairment at the lowest level at which

individual cash flows can be identified. When evaluating these

long-lived assets for potential impairment, we first compare

the carrying amount of the asset group to the asset group’s

estimated future cash flows (undiscounted and without interest

charges). If the estimated future cash flows are less than the

carrying amount of the asset group, an impairment loss calcula-

tion is prepared. The impairment loss calculation compares

the carrying amount of the asset group to the asset group’s

estimated future cash flows (discounted and with interest

charges). If required, an impairment loss is recorded for the

portion of the asset group’s carrying value that exceeds the

asset group’s estimated future cash flows (discounted and

with interest charges). Our long-lived asset impairment loss

calculation contains uncertainty since we must use judgment

to estimate each asset group’s future sales, profitability and

cash flows. When preparing these estimates, we consider

historical results and current operating trends and our consoli-

dated sales, profitability and cash flow results and forecasts.

These estimates can be affected by a number of factors

including, but not limited to, general economic conditions,

efforts of third-party organizations to reduce their prescription

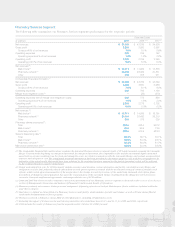

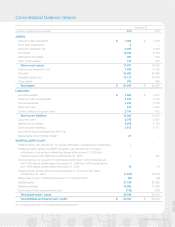

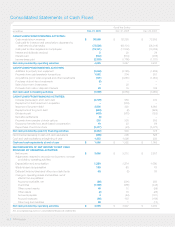

Following is a summary of our significant contractual obligations as of December 31, 2009:

Payments Due by Period

2011 2013

in millions Total 2010 to 2012 to 2014 Thereafter

Operating leases $ 26,913 $ 2,094 $ 3,830 $ 3,512 $ 17,477

Leases from discontinued operations 150 5 48 23 74

Long-term debt 10,706 2,102 2,103 551 5,950

Interest payments on long-term debt (1) 7,307 559 1,058 980 4,710

Other long-term liabilities reflected in

our consolidated balance sheet 273 76 50 50 97

Capital lease obligations 154 2 7 9 136

$ 45,503 $ 4,838 $ 7,096 $ 5,125 $ 28,444

(1) Interest payments on long-term debt are calculated on outstanding balances and interest rates in effect on December 31, 2009.

Critical Accounting Policies

We prepare our consolidated financial statements in confor-

mity with generally accepted accounting principles, which

require management to make certain estimates and apply

judgment. We base our estimates and judgments on historical

experience, current trends and other factors that management

believes to be important at the time the consolidated financial

statements are prepared. On a regular basis, we review our

accounting policies and how they are applied and disclosed

in our consolidated financial statements. While we believe the

historical experience, current trends and other factors consid-

ered, support the preparation of our consolidated financial

statements in conformity with generally accepted accounting

principles, actual results could differ from our estimates, and

such differences could be material.

Our significant accounting policies are discussed in Note 1 to

our consolidated financial statements. We believe the following

accounting policies include a higher degree of judgment and/or

complexity and, thus, are considered to be critical accounting

policies. The critical accounting policies discussed later in this

document are applicable to each of our business segments. We

have discussed the development and selection of our critical

accounting policies with the Audit Committee of our Board of

Directors and the Audit Committee has reviewed our disclo-

sures relating to them.

GOODWILL AND INTANGIBLE ASSETS

Identifiable intangible assets consist primarily of trademarks,

client contracts and relationships, favorable and unfavorable

leases and covenants not to compete. These intangible assets

arise primarily from the allocation of the purchase price of

businesses acquired to identifiable intangible assets based on

their respective fair market values at the date of acquisition.

CVS Caremark

36