Berkshire Hathaway 1999 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 1999 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

48

Management's Discussion (continued)

Insurance Segments - Underwriting (continued)

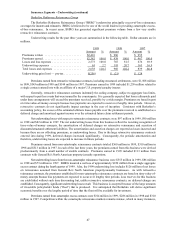

Berkshire Hathaway Reinsurance Group (Continued)

makes premium rates inadequate or coverage conditions unacceptable. As a result, BHRG has accepted relatively few

new arrangements. However, it is expected that this business will still produce meaningful amounts of earned premiums

during 2000.

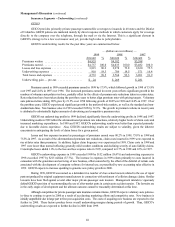

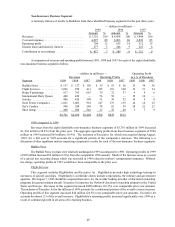

Net underwriting gains from catastrophe reinsurance were $196 million in 1999, $155 million in 1998 and

$283 million in 1997. Catastrophe losses incurred in 1999 and 1998 were relatively minor. Significant exposure to losses

remains with respect to contracts that are in-force at year-end 1999, especially with respect to a major earthquake in

California or a hurricane affecting the U.S. Future periodic underwriting results of this business are subject to extreme

volatility. However, Berkshire’s management is willing to accept volatility in reported results, provided there is a

reasonable prospect of long-term profitability.

Berkshire Hathaway Direct Insurance Group

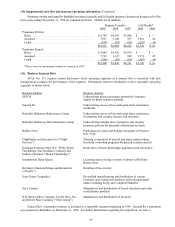

The Berkshire Hathaway Direct Insurance Group is comprised of a wide variety of smaller property/casualty

businesses. These businesses include: National Indemnity Company's traditional commercial motor vehicle and

specialty risk operations; six companies collectively referred to as "homestate" operations that provide primarily standard

commercial coverages to insureds in an increasing number of states; Cypress Insurance Company, a provider of workers'

compensation insurance in California and other states; Central States Indemnity Company, a provider of credit card

credit insurance to individuals nationwide through financial institutions; Kansas Bankers Surety Company, an insurer

for primarily small and medium size banks located in the midwest; and Berkshire Hathaway International, a London-

based writer of personal and commercial auto insurance.

Collectively, direct insurance businesses produced earned premiums of $262 million in 1999, $328 million in

1998 and $312 million in 1997. The decrease in premiums earned in 1999 compared to 1998 was essentially attributed

to the credit card and international auto businesses, whereas the comparative increase in premiums earned in 1998 over

1997 was largely due to those same operations. Net underwriting gains of the direct businesses totaled $22 million in

1999, $17 million in 1998 and $52 million in 1997. The increase in underwriting profits in 1999 over 1998 was due

primarily to lower net losses from the international auto business. The decline in net underwriting gains in 1998 from

1997 was principally due to lower profits from the specialty risk operations.

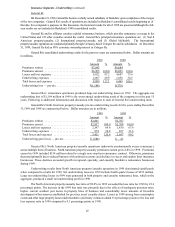

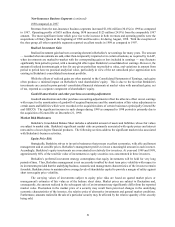

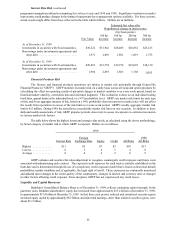

Insurance Segments - Investment Income

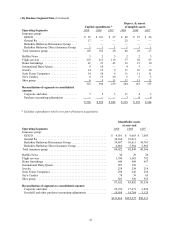

Following is a summary of the insurance segments net investment income for the past three years.

(dollars in millions)

1999 1998 1997

Investment income before taxes ..................................... $2,482 $974 $882

Applicable income taxes and minority interest .......................... 718 243 178

Investment income after taxes and minority interest ..................... $1,764 $731 $704

Investment income before taxes from the insurance operations in 1999 includes $1,328 million from General

Re, which was acquired by Berkshire on December 21, 1998. Invested assets grew by approximately $25 billion as a

result of the General Re acquisition. At December 31, 1999, cash and invested assets totaled approximately $72 billion.

Excluding the impact of General Re, net investment income in 1999 grew 18.5% over amounts earned in 1998. In 1998,

net investment income exceeded 1997 by 10.4%.

Berkshire’s insurance businesses generate large amounts of investment income derived from shareholder

capital, as well as policyholder float. Float represents an estimate of the amount of funds ultimately payable to

policyholders that is available for investment. Float denotes the sum of net loss and loss adjustment expense reserves,

unearned premiums, and funds held under reinsurance agreements, less premiums receivable, deferred acquisition costs,

deferred charges on retroactive reinsurance and prepaid income taxes. The aggregate float was approximately $25.3

billion at December 31, 1999 and $22.8 billion at December 31, 1998. The acquisition of General Re increased float

by approximately $14.9 billion.

Income taxes and minority interest as a percentage of investment income before taxes were 28.9% for 1999,

24.9% for 1998 and 20.2% for 1997. The increase in the rates reflects an increase in the proportion of taxable interest

income relative to the amounts of dividend and tax-exempt interest, which are effectively taxed at lower rates. Minority

interest applicable to investment income in 1999 also increased due to amounts related to investment income of Cologne

Re.