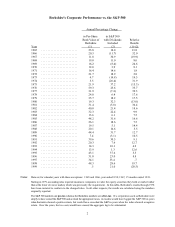

Berkshire Hathaway 1999 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 1999 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

12

Acquisition Accounting

Once again, I would like to make some comments about accounting, in this case about its application to

acquisitions. This is currently a very contentious topic and, before the dust settles, Congress may even intervene (a truly

terrible idea).

When a company is acquired, generally accepted accounting principles (“GAAP”) currently condone two very

different ways of recording the transaction: “purchase” and “pooling.” In a pooling, stock must be the currency; in a

purchase, payment can be made in either cash or stock. Whatever the currency, managements usually detest purchase

accounting because it almost always requires that a “goodwill” account be established and subsequently written off —

a process that saddles earnings with a large annual charge that normally persists for decades. In contrast, pooling avoids

a goodwill account, which is why managements love it.

Now, the Financial Accounting Standards Board (“FASB”) has proposed an end to pooling, and many CEOs are

girding for battle. It will be an important fight, so we’ll venture some opinions. To begin with, we agree with the many

managers who argue that goodwill amortization charges are usually spurious. You’ll find my thinking about this in the

appendix to our 1983 annual report, which is available on our website, and in the Owner’s Manual on pages 55 - 62.

For accounting rules to mandate amortization that will, in the usual case, conflict with reality is deeply

troublesome: Most accounting charges relate to what’s going on, even if they don’t precisely measure it. As a n

example, depreciation charges can’t with precision calibrate the decline in value that physical assets suffer, but these

charges do at least describe something that is truly occurring: Physical assets invariably deteriorate. Correspondingly,

obsolescence charges for inventories, bad debt charges for receivables and accruals for warranties are among the charges

that reflect true costs. The annual charges for these expenses can’t be exactly measured, but the necessity for estimating

them is obvious.

In contrast, economic goodwill does not, in many cases, diminish. Indeed, in a great many instances — perhaps

most — it actually grows in value over time. In character, economic goodwill is much like land: The value of both

assets is sure to fluctuate, but the direction in which value is going to go is in no way ordained. At See’s, for example,

economic goodwill has grown, in an irregular but very substantial manner, for 78 years. And, if we run the business

right, growth of that kind will probably continue for at least another 78 years.

To escape from the fiction of goodwill charges, managers embrace the fiction of pooling. This accounting

convention is grounded in the poetic notion that when two rivers merge their streams become indistinguishable. Under

this concept, a company that has been merged into a larger enterprise has not been “purchased” (even though it will

often have received a large “sell-out” premium). Consequently, no goodwill is created, and those pesky subsequent

charges to earnings are eliminated. Instead, the accounting for the ongoing entity is handled as if the businesses had

forever been one unit.

So much for poetry. The reality of merging is usually far different: There is indisputably an acquirer and an

acquiree, and the latter has been “purchased,” no matter how the deal has been structured. If you think otherwise, just

ask employees severed from their jobs which company was the conqueror and which was the conquered. You will find

no confusion. So on this point the FASB is correct: In most mergers, a purchase has been made. Yes, there are some

true “mergers of equals,” but they are few and far between.

Charlie and I believe there’s a reality-based approach that should both satisfy the FASB, which correctly wishes

to record a purchase, and meet the objections of managements to nonsensical charges for diminution of goodwill. We

would first have the acquiring company record its purchase price — whether paid in stock or cash — at fair value. In

most cases, this procedure would create a large asset representing economic goodwill. We would then leave this asset

on the books, not requiring its amortization. Later, if the economic goodwill became impaired, as it sometimes would,

it would be written down just as would any other asset judged to be impaired.

If our proposed rule were to be adopted, it should be applied retroactively so that acquisition accounting would

be consistent throughout America — a far cry from what exists today. One prediction: If this plan were to take effect,

managements would structure acquisitions more sensibly, deciding whether to use cash or stock based on the real

consequences for their shareholders rather than on the unreal consequences for their reported earnings.

* * * * * * * * * * * *