Supercuts 2007 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2007 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

expire within ten years from the grant date. The Company utilizes an option-pricing model to estimate the fair value of options at their grant

date. The Company generally recognizes compensation expense for its stock-based compensation awards on a straight-line basis over the five-

year vesting period. Awards granted do not contain acceleration of vesting terms for retirement eligible recipients. The company

’s primary

employee stock-based compensation grant occurs during the fourth quarter.

Prior to July 1, 2003, the Company accounted for its stock-based awards using the intrinsic value method under the recognition and

measurement principles of Accounting Principles Board Opinion No. 25, Accounting for Stock Issued to Employees (APB No. 25) and related

Interpretations. Under the provisions of APB No. 25, no stock-based employee compensation cost was reflected in net income, as all options

granted under those plans had an exercise price equal to the market value of the underlying stock on the date of grant.

Effective July 1, 2003, the Company adopted the fair value recognition provisions of SFAS No. 123, Accounting for Stock-Based

Compensation

(SFAS No. 123), as amended, using the prospective transition method. Under the prospective method of adoption, compensation

cost is recognized on all stock-

based awards granted, modified or settled subsequent to July 1, 2003. Under this approach, fiscal years 2005 and

2004 compensation expense is less than it would have been had the fair value recognition provisions of SFAS No. 123 been applied from its

original effective date because the fair value of the options vesting during the year which were granted prior to fiscal year 2004 are not

recognized as expense in the Consolidated Statement of Operations. Options granted in fiscal years prior to the adoption of the fair value

recognition provisions continued to be accounted for under APB No. 25 for fiscal years 2005 and 2004. The adoption of the fair value

recognition provisions for stock options increased the Company’s fiscal year 2005 compensation expense by $0.4 million (related to

recognizing compensation expense over the vesting period of options granted after July 1, 2003).

Effective July 1, 2005, the Company adopted SFAS No. 123 (revised 2004), Share-Based Payment (SFAS No. 123R), using the modified

prospective method of application. Under this method, compensation expense is recognized both for (i) awards granted, modified or settled

subsequent to July 1, 2003 and (ii) the remaining vesting periods of awards issued prior to July 1, 2003. The impact of adopting SFAS

No. 123R during fiscal years 2007 and 2006 was an increase in compensation expense of $1.0 and $2.7 million ($0.7 and $1.7 million after

tax), respectively, and a reduction of $0.01 and $0.04 for both basic and diluted earnings per share for fiscal years 2007 and 2006, respectively.

Compensation expense recorded during fiscal years 2007 and 2006 includes $3.9 and $2.3 million, respectively, related to awards issued

subsequent to July 1, 2003 and $1.0 and $2.7 million, respectively, related to unvested awards previously being accounted for on the intrinsic

value method of accounting.

Total compensation cost for stock-based payment arrangements totaled $4.9, $4.9 and $1.2 million ($3.2 and $4.1 and $0.8 million after

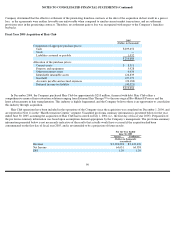

tax) for the fiscal years ended June 30, 2007, 2006 and 2005, respectively. SFAS No. 123R also requires that the cash retained as a result of the

tax deductibility of increases in the value of stock-

based arrangements be presented as a cash inflow from financing activity in the Consolidated

Statement of Cash Flows. The amount presented as a financing activity for fiscal years 2007 and 2006 was $4.5 and $4.6 million, respectively.

Prior to fiscal year 2006, and the Company’s adoption of SFAS No. 123R, the tax benefit realized upon the exercise of stock options was

presented as an operating activity (included within accrued expenses) and totaled $9.0 million for fiscal year 2005.

81