Supercuts 2004 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2004 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Table of Contents

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS, CONTINUED

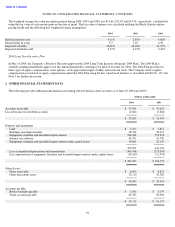

Property and Equipment:

Property and equipment are carried at cost, less accumulated depreciation and amortization. Depreciation and amortization of property and

equipment are computed on the straight-line method over estimated useful asset lives (30 to 39 years for buildings and improvements and

five to ten years for equipment, furniture, software and leasehold improvements).

The Company capitalizes both internal and external costs of developing or obtaining computer software for internal use. Costs incurred to

develop internal-use software during the application development stage are capitalized, while data conversion, training and maintenance

costs associated with internal-use software are expensed as incurred. At June 30, 2004 and 2003, the net book value of capitalized software

costs was $21.6 million. Amortization expense related to capitalized software was $5.8, $5.8 and $5.5 million in fiscal years 2004, 2003 and

2002, respectively, which has been determined based on an estimated useful life of five or seven years.

Expenditures for maintenance and repairs and minor renewals and betterments which do not improve or extend the life of the respective

assets are expensed. All other expenditures for renewals and betterments are capitalized. The assets and related depreciation and

amortization accounts are adjusted for property retirements and disposals with the resulting gain or loss included in operations. Fully

depreciated/amortized assets remain in the accounts until retired from service.

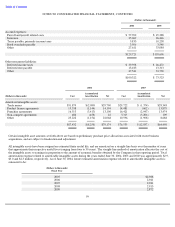

Goodwill:

Effective July 1, 2001, the Company ceased all amortization of goodwill balances. Goodwill is tested for impairment annually or at the time

of a triggering event in accordance with the provisions of Statement of Financial Accounting Standards (FAS) No. 142, “Goodwill and

Other Intangible Assets.” Fair values are estimated based on the Company’s best estimate of the expected present value of future cash flows

and compared with the corresponding carrying value of the reporting unit, including goodwill. The Company generally considers its various

concepts to be reporting units when it tests for goodwill impairment because that is where the Company believes goodwill naturally resides.

During the third quarter of each of the three fiscal years in the period ending June 30, 2004, goodwill was tested for impairment in this

manner. The estimated fair value of the reporting units exceeded their carrying amounts, indicating no impairment of goodwill.

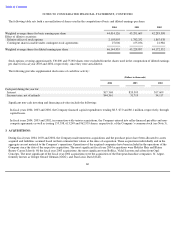

Asset Impairment Assessments:

The Company reviews long-lived assets for impairment at the salon level annually or if events or circumstances indicate that the carrying

value of such assets may not be fully recoverable. Impairment is evaluated based on the sum of undiscounted estimated future cash flows

expected to result from use of the assets compared to its carrying value. If an impairment is recognized, the carrying value of the impaired

asset is reduced to its fair value, based on discounted estimated future cash flows.

During fiscal years 2004, 2003 and 2002, the Company tested its long-lived assets for impairment and recognized impairment charges

related to the carrying value of certain salons’ property and equipment located primarily in North America of $3.2, $3.1 and $1.3 million,

respectively. None of the impaired salon assets were held for sale. Impairment charges are included in depreciation related to company-

owned salons in the Consolidated Statement of Operations.

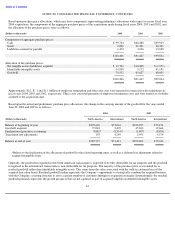

Deferred Rent:

The Company’s operating lease agreements include certain escalation provisions. Accounting principles generally accepted in the United

States of America require rent expense to be recognized on a straight-line basis over the lease term. The difference between the rent due

under the stated terms of the lease compared to that of the straight-

line basis is recorded as deferred rent within other noncurrent liabilities in

the Consolidated Balance Sheet.

54