Supercuts 2004 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2004 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Table of Contents

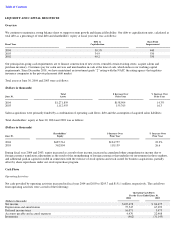

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

The primary market risk exposure of the Company relates to changes in interest rates in connection with its debt, some of which bears interest

at floating rates based on LIBOR plus an applicable borrowing margin. Additionally, the Company is exposed to foreign currency translation

risk related to its net investments in its foreign subsidiaries. The Company has established policies and procedures that govern the management

of these exposures. By policy, the Company does not enter into such contracts for the purpose of speculation. The following details the

Company’s policies and use of financial instruments.

Interest Rate Risk:

The Company has established an interest rate management policy that attempts to minimize its overall cost of debt, while taking into

consideration the earnings implications associated with the volatility of short-term interest rates. As part of this policy, the Company has

elected to maintain a combination of floating and fixed rate debt. Considering the Company’s policy of maintaining variable rate debt

instruments, a one percent change in interest rates may impact the Company’s interest expense by approximately $1.0 million. As of June 30,

2004 and 2003, the Company had the following outstanding debt balances:

In addition, the Company has entered into the following financial instruments:

Interest Rate Swap Contracts:

The Company manages its interest rate risk by balancing the amount of fixed and floating rate debt. On occasion, the Company uses interest

rate swaps to further mitigate the risk associated with changing interest rates and to maintain its desired balances of fixed and floating rate debt.

Generally, the terms of the interest rate swap agreements contain quarterly settlement dates based on the notional amounts of the swap

contracts.

(Pay fixed rates, receive variable rates)

The Company had interest rate swap contracts that pay fixed rates of interest and receive variable rates of interest (based on the three-month

LIBOR rate) on notional amounts of indebtedness of $11.8 million at June 30, 2004 and 2003. These swaps are being accounted for as cash

flow swaps. During fiscal year 2003, the $11.8 million interest rate swap was redesignated from a hedge of variable rate operating lease

obligations to hedge of a portion of the interest payments associated with the Company’s long-term financing program. The redesignation was

the result of the Company exercising its right to purchase the property under the variable rate operating lease. See the discussion in Note 5 to

the Consolidated Financial Statements for further explanation.

(Pay variable rates, receive fixed rates)

The Company has interest rate swap contracts that pay variable rates of interest (based on the three-month and six-month LIBOR rates plus a

credit spread) and receive fixed rates of interest on an aggregate $81.0 and $88.5 million notional amount at June 30, 2004 and 2003,

respectively, with maturation dates between July 2005 and March 2009. These swaps were designated as hedges of a portion of the Company’s

senior term notes and are being accounted for as fair value swaps.

During the second quarter of fiscal year 2003, the Company terminated a portion of its $40.0 million interest rate swap contract, thereby

lowering the aggregate notional amount by $20.0 million. See Note 5 to the Consolidated Financial Statements for further discussion.

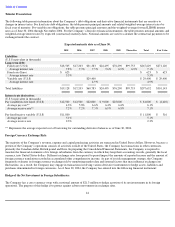

43

June 30,

(Dollars in thousands)

2004

2003

Fixed rate debt

$

271,743

$

278,957

Floating rate debt

29,400

22,800

$

301,143

$

301,757