Logitech 2006 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2006 Logitech annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

Accounting for Income Taxes

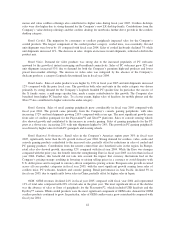

Logitech operates in multiple jurisdictions and its profits are taxed pursuant to the tax laws of these

jurisdictions. The Company’s effective tax rate may be affected by the changes in or interpretations of tax laws in

any given jurisdiction, utilization of net operating loss and tax credit carry forwards, changes in geographical mix

of income and expense, and changes in management’s assessment of matters such as the ability to realize

deferred tax assets. As a result of these considerations, the Company must estimate income taxes in each of the

jurisdictions in which it operates. This process involves estimating actual current tax exposure together with

assessing temporary differences resulting from different treatment of items for tax and accounting purposes.

These differences result in deferred tax assets and liabilities, which are included in the consolidated balance

sheet. The Company must then assess the likelihood that its deferred tax assets will be recovered from future

taxable income, and to the extent that recovery is not likely, a valuation allowance is established for any amounts

the Company believes will not be recoverable. Establishing or increasing a valuation allowance increases income

tax expense in such period, while releasing a valuation allowance reduces income tax expense or increases

additional paid-in capital in certain circumstances in such period.

Significant management judgment is required in determining the provision for income taxes, the deferred

tax assets and liabilities and any valuation allowance recorded against the net deferred tax assets. Logitech has

recorded a valuation allowance at March 31, 2006 due to uncertainties related to its ability to utilize some of the

deferred tax assets before they expire. The valuation allowance is based on estimates of future taxable income by

jurisdiction in which the Company operates and the period over which the deferred tax assets will be recoverable.

In the event that actual results differ from these estimates or the estimates are adjusted in future periods, the

Company may need to release a valuation allowance or establish an additional valuation allowance which could

materially impact the Company’s financial position and results of operations in the period when the valuation

allowances are adjusted.

In addition, the Company is subject to examination by various taxing authorities. The Company believes it

has adequately provided in the financial statements for additional taxes that it estimates may be required to be

paid as a result of such examinations. If the payment ultimately proves to be unnecessary, the reversal of the tax

liabilities would result in tax benefits being recognized in the period the Company determines the liabilities are

no longer necessary. If a final tax assessment exceeds the Company’s estimate of tax liabilities, an additional

charge to expense will result. See Note 10—“Income Taxes” for further discussion.

Valuation of Long-Lived Assets

The Company reviews long-lived assets, such as investments, property, plant and equipment, and goodwill

and other intangible assets for impairment whenever events indicate that the carrying amount of these assets

might not be recoverable. Factors considered as important which could require it to review an asset for

impairment include the following:

• significant underperformance relative to historical or projected future operating results;

• significant changes in the manner of its use of the acquired assets or the strategy for its overall business;

• significant negative industry or economic trends;

• significant decline in its stock price for a sustained period; and

• its market capitalization relative to net book value.

Recoverability of investments, property, plant and equipment, and other intangible assets is measured by

comparing the projected undiscounted cash flows the asset is expected to generate with its carrying amount. If an

asset is considered impaired, the impairment to be recognized is measured by the amount by which the carrying

amount of the asset exceeds its fair value.

The Company evaluates goodwill for impairment on an annual basis and whenever events or changes in

circumstances indicate that the carrying amount may not be recoverable from its estimated future cash flows.

36