Dollar General 2009 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2009 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

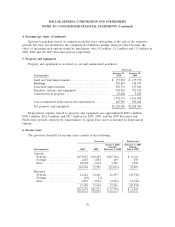

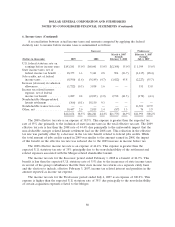

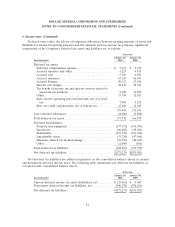

DOLLAR GENERAL CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

1. Basis of presentation and accounting policies (Continued)

prove to be inaccurate, the resulting adjustments could be material to the Company’s future financial

results.

Management estimates

The preparation of financial statements and related disclosures in conformity with accounting

principles generally accepted in the United States requires management to make estimates and

assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets

and liabilities at the date of the consolidated financial statements and the reported amounts of

revenues and expenses during the reporting periods. Actual results could differ from those estimates.

Accounting standards

In June 2009 the Financial Accounting Standards Board (‘‘FASB’’) issued a new accounting

standard which established the FASB Accounting Standards Codification (‘‘ASC’’) as the source of

authoritative U.S. GAAP recognized by the FASB to be applied by nongovernmental entities. Rules and

interpretive releases of the Securities and Exchange Commission (‘‘SEC’’) under authority of federal

securities laws are also sources of authoritative GAAP for SEC registrants, including the Company. On

September 15, 2009, the effective date of this standard, the ASC superseded all then-existing non-SEC

accounting and reporting standards. All other nongrandfathered non-SEC accounting literature not

included in the ASC became nonauthoritative. The adoption of this statement did not have a material

effect on the Company’s consolidated financial statements.

In June 2009 the FASB issued a new accounting standard relating to variable interest entities. This

standard amends previous standards and requires an enterprise to perform an analysis to determine

whether the enterprise’s variable interest or interests give it a controlling financial interest in a variable

interest entity, specifies updated criteria for determining the primary beneficiary, requires ongoing

reassessments of whether an enterprise is the primary beneficiary of a variable interest entity,

eliminates the quantitative approach previously required for determining the primary beneficiary of a

variable interest entity, amends certain guidance for determining whether an entity is a variable interest

entity, requires enhanced disclosures about an enterprise’s involvement in a variable interest entity, and

includes other provisions. This standard will be effective as of the beginning of the Company’s first

interim and annual reporting periods that begin after November 15, 2009. Earlier application is

prohibited. This standard is not expected to have a material effect on the consolidated financial

statements.

During the second quarter of 2009 the Company adopted the ASC Subsequent Events Topic. The

objective of this topic is to establish general standards of accounting for and disclosures of events that

occur after the balance sheet date but before financial statements are issued or are available to be

issued. In particular, this topic sets forth the period after the balance sheet date during which

management of a reporting entity should evaluate events or transactions that may occur for potential

recognition or disclosure in the financial statements, the circumstances under which an entity should

recognize events or transactions occurring after the balance sheet date in its financial statements, and

the disclosures that an entity should make about events or transactions that occurred after the balance

sheet date. In February 2010 minor modifications were made to this guidance. The adoption of these

standards has not had a material effect on the Company’s consolidated financial statements.

74