Dollar General 2009 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2009 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

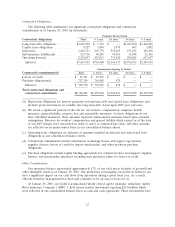

Prepayments. The senior secured credit agreement for the Term Loan Facility requires us to

prepay outstanding term loans, subject to certain exceptions, with:

• 50% of our annual excess cash flow (as defined in the credit agreement) which will be reduced

to 25% and 0% if we achieve and maintain a total net leverage ratio of 6.0 to 1.0 and 5.0 to 1.0,

respectively;

• 100% of the net cash proceeds of all non-ordinary course asset sales or other dispositions of

property in excess of $25.0 million in the aggregate and subject to our right to reinvest the

proceeds; and

• 100% of the net cash proceeds of any incurrence of debt, other than proceeds from debt

permitted under the senior secured credit agreement.

The mandatory prepayments discussed above will be applied to the Term Loan Facility as directed

by the senior secured credit agreement. Through January 29, 2010, no prepayments have been required

under the prepayment provisions listed above. The Term Loan Facility can be prepaid in whole or in

part at any time.

In addition, the senior secured credit agreement for the ABL Facility requires us to prepay the

ABL Facility, subject to certain exceptions, as follows:

• With 100% of the net cash proceeds of all non-ordinary course asset sales or other dispositions

of revolving facility collateral (as defined below) in excess of $1.0 million in the aggregate and

subject to our right to reinvest the proceeds; and

• To the extent such extensions of credit exceed the then current borrowing base (as defined in

the senior secured credit agreement for the ABL Facility).

The mandatory prepayments discussed above will be applied to the ABL Facility as directed by the

senior secured credit agreement for the ABL Facility. Through January 29, 2010, no prepayments have

been required under the prepayment provisions listed above.

An event of default under the senior secured credit agreements will occur upon a change of

control as defined in the senior secured credit agreements governing our Credit Facilities. Upon an

event of default, indebtedness under the Credit Facilities may be accelerated, in which case we will be

required to repay all outstanding loans plus accrued and unpaid interest and all other amounts

outstanding under the Credit Facilities.

Amortization. Beginning September 30, 2009, we were required to repay installments on the loans

under the Term Loan Facility in equal quarterly principal amounts in an aggregate amount per annum

equal to 1% of the original principal amount. During 2009, we paid two such quarterly installments

totaling $11.5 million. Due to the $325.0 million voluntary prepayment of the Term Loan Facility

discussed above, no further quarterly principal installments will be required prior to maturity of the

Term Loan on July 6, 2014. There is no amortization under the ABL Facility. The entire principal

amounts (if any) outstanding under the ABL Facility are due and payable in full at maturity, on July 6,

2013, on which day the commitments thereunder will terminate.

Guarantee and Security. All obligations under the Credit Facilities are unconditionally guaranteed

by substantially all of our existing and future domestic subsidiaries (excluding certain immaterial

subsidiaries and certain subsidiaries designated by us under our senior secured credit agreements as

‘‘unrestricted subsidiaries’’), referred to, collectively, as U.S. Guarantors.

42