Chevron 2014 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2014 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

A differential in crude oil prices exists between high-quality (high-gravity, low-sulfur) crudes and those of lower quality

(low-gravity, high-sulfur). The amount of the differential in any period is associated with the supply of heavy crude versus

the demand, which is a function of the capacity of refineries that are able to process this lower quality feedstock into light

products (motor gasoline, jet fuel, aviation gasoline and diesel fuel). After peaking early in second quarter 2014, the

differential has eased in North America as refinery crude runs remained at or above record levels. Outside of North America,

easing of geopolitical tensions and continued expansion of supply of light sweet crudes has pressured light sweet crude prices

relative to those for heavier, more sour crudes.

Chevron produces or shares in the production of heavy crude oil in California, Indonesia, the Partitioned Zone between Saudi

Arabia and Kuwait, Venezuela and in certain fields in Angola, China and the United Kingdom sector of the North Sea. (See

page 19 for the company’s average U.S. and international crude oil realizations.)

In contrast to price movements in the global market for crude oil, price changes for natural gas in many regional markets are

more closely aligned with supply-and-demand conditions in those markets. Fluctuations in the price of natural gas in the

United States are closely associated with customer demand relative to the volumes produced and stored in North America. In

the United States, prices at Henry Hub averaged $4.28 per thousand cubic feet (MCF) during 2014, compared with $3.70

during 2013. As of mid-February 2015, the Henry Hub spot price was $2.73 per MCF.

Outside the United States, price changes for natural gas depend on a wide range of supply, demand, regulatory and

commercial factors. In some locations, Chevron is investing in long-term projects to install infrastructure to produce and

liquefy natural gas for transport by tanker to other markets. The company’s contract prices for liquefied natural gas (LNG)

are typically linked to crude oil prices. Chevron’s international natural gas realizations averaged $5.78 per MCF during 2014,

compared with $5.91 per MCF during 2013. (See page 19 for the company’s average natural gas realizations for the U.S. and

international regions.)

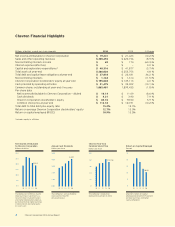

0

5500

4400

1100

2200

3300

Net Natural Gas Production*

Millions of cubic feet per day

United States

International

*Includes equity in affiliates.

1110 12 13 14

5,167

0

2000

1600

1200

800

400

Net Liquids Production*

Thousands of barrels per day

United States

International

*Includes equity in affiliates.

1110 12 13 14

1,709

0.0

12.5

7.5

5.0

10.0

2.5

Net Proved Reserves

Billions of BOE

United States

Other Americas

Africa

Asia

Australia

Europe

Affiliates

11.1

10 11

12

13

14

Net Proved Reserves

Liquids vs. Natural Gas

Billions of BOE

1110 12 13 14

11.1

Natural Gas

Liquids

12.5

7.5

0.0

10.0

5.0

2.5

The company’s worldwide net oil-equivalent production in 2014 averaged 2.571 million million barrels per day. About one-

fifth of the company’s net oil-equivalent production in 2014 occurred in the OPEC-member countries of Angola, Nigeria,

Venezuela and the Partitioned Zone between Saudi Arabia and Kuwait. OPEC quotas had no effect on the company’s net

crude oil production in 2014 or 2013. At their November 2014 meeting, members of OPEC supported maintaining the current

production quota of 30 million barrels per day, which has been in effect since December 2008.

The company estimates that oil-equivalent production in 2015 will be flat to 3 percent growth compared to 2014. This

estimate is subject to many factors and uncertainties, including the duration of the low price environment that began in

second-half 2014; quotas that may be imposed by OPEC; price effects on entitlement volumes; changes in fiscal terms or

restrictions on the scope of company operations; delays in construction, start-up or ramp-up of projects; fluctuations in

demand for natural gas in various markets; weather conditions that may shut in production; civil unrest; changing

geopolitics; delays in completion of maintenance turnarounds; greater-than-expected declines in production from mature

12 Chevron Corporation 2014 Annual Report