Boeing 2014 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2014 Boeing annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

87

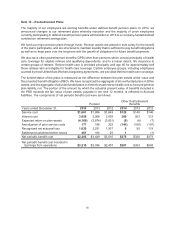

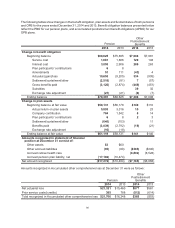

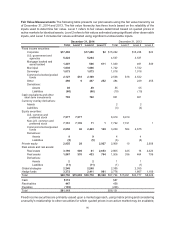

The estimated amount that will be amortized from Accumulated other comprehensive loss into net periodic

benefit cost during the year ended December 31, 2015 is as follows:

Pension

Other

Postretirement

Benefits

Recognized net actuarial loss $1,581 $27

Amortization of prior service costs/(credits) 193 (134)

Total $1,774 ($107)

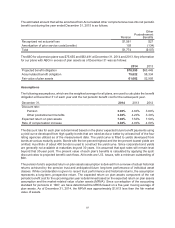

The ABO for all pension plans was $75,655 and $63,491 at December 31, 2014 and 2013. Key information

for our plans with ABO in excess of plan assets as of December 31 was as follows:

2014 2013

Projected benefit obligation $78,358 $63,445

Accumulated benefit obligation 75,622 58,334

Fair value of plan assets 61,082 52,905

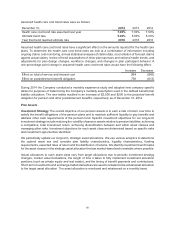

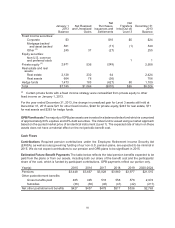

Assumptions

The following assumptions, which are the weighted average for all plans, are used to calculate the benefit

obligation at December 31 of each year and the net periodic benefit cost for the subsequent year.

December 31, 2014 2013 2012

Discount rate:

Pension 3.90% 4.80% 3.80%

Other postretirement benefits 3.50% 4.20% 3.30%

Expected return on plan assets 7.00% 7.50% 7.50%

Rate of compensation increase 3.80% 4.00% 4.00%

The discount rate for each plan is determined based on the plans’ expected future benefit payments using

a yield curve developed from high quality bonds that are rated as Aa or better by at least half of the four

rating agencies utilized as of the measurement date. The yield curve is fitted to yields developed from

bonds at various maturity points. Bonds with the ten percent highest and the ten percent lowest yields are

omitted. A portfolio of about 400 bonds is used to construct the yield curve. Since corporate bond yields

are generally not available at maturities beyond 30 years, it is assumed that spot rates will remain level

beyond that 30-year point. The present value of each plan’s benefits is calculated by applying the spot/

discount rates to projected benefit cash flows. All bonds are U.S. issues, with a minimum outstanding of

$50.

The pension fund’s expected return on plan assets assumption is derived from a review of actual historical

returns achieved by the pension trust and anticipated future long-term performance of individual asset

classes. While consideration is given to recent trust performance and historical returns, the assumption

represents a long-term, prospective return. The expected return on plan assets component of the net

periodic benefit cost for the upcoming plan year is determined based on the expected return on plan assets

assumption and the market-related value of plan assets (MRVA). Since our adoption of the accounting

standard for pensions in 1987, we have determined the MRVA based on a five-year moving average of

plan assets. As of December 31, 2014, the MRVA was approximately $1,813 less than the fair market

value of assets.