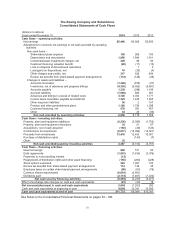

Boeing 2014 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2014 Boeing annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

44

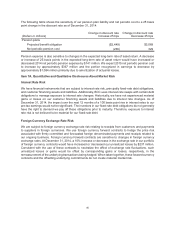

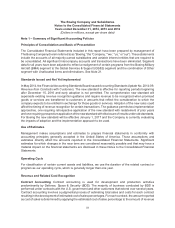

a number of our fixed price development contracts are in a reach-forward loss position. Changes to

estimated losses are recorded immediately in earnings.

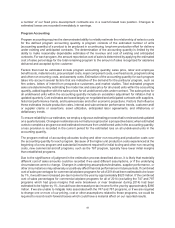

Program Accounting

Program accounting requires the demonstrated ability to reliably estimate the relationship of sales to costs

for the defined program accounting quantity. A program consists of the estimated number of units

(accounting quantity) of a product to be produced in a continuing, long-term production effort for delivery

under existing and anticipated contracts. The determination of the accounting quantity is limited by the

ability to make reasonably dependable estimates of the revenue and cost of existing and anticipated

contracts. For each program, the amount reported as cost of sales is determined by applying the estimated

cost of sales percentage for the total remaining program to the amount of sales recognized for airplanes

delivered and accepted by the customer.

Factors that must be estimated include program accounting quantity, sales price, labor and employee

benefit costs, material costs, procured part costs, major component costs, overhead costs, program tooling

and other non-recurring costs, and warranty costs. Estimation of the accounting quantity for each program

takes into account several factors that are indicative of the demand for the particular program, such as

firm orders, letters of intent from prospective customers, and market studies. Total estimated program

sales are determined by estimating the model mix and sales price for all unsold units within the accounting

quantity, added together with the sales prices for all undelivered units under contract. The sales prices for

all undelivered units within the accounting quantity include an escalation adjustment for inflation that is

updated quarterly. Cost estimates are based largely on negotiated and anticipated contracts with suppliers,

historical performance trends, and business base and other economic projections. Factors that influence

these estimates include production rates, internal and subcontractor performance trends, customer and/

or supplier claims or assertions, asset utilization, anticipated labor agreements, and inflationary or

deflationary trends.

To ensure reliability in our estimates, we employ a rigorous estimating process that is reviewed and updated

on a quarterly basis. Changes in estimates are normally recognized on a prospective basis; when estimated

costs to complete a program exceed estimated revenues from undelivered units in the accounting quantity,

a loss provision is recorded in the current period for the estimated loss on all undelivered units in the

accounting quantity.

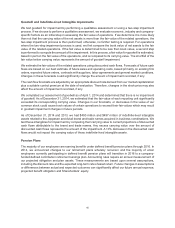

The program method of accounting allocates tooling and other non-recurring and production costs over

the accounting quantity for each program. Because of the higher unit production costs experienced at the

beginning of a new program and substantial investment required for initial tooling and other non-recurring

costs, new commercial aircraft programs, such as the 787 program, typically have lower initial margins

than established programs.

Due to the significance of judgment in the estimation process described above, it is likely that materially

different cost of sales amounts could be recorded if we used different assumptions, or if the underlying

circumstances were to change. Changes in underlying assumptions/estimates, supplier performance, or

other circumstances may adversely or positively affect financial performance in future periods. If combined

cost of sales percentages for commercial airplane programs for all of 2014 had been estimated to be lower

by 1%, it would have increased pre-tax income for the year by approximately $520 million. If the combined

cost of sales percentages for commercial airplane programs for all of 2014 (excluding the 747 and 787

programs which had gross margins that were breakeven or near breakeven during 2014) had been

estimated to be higher by 1%, it would have decreased pre-tax income for the year by approximately $360

million. If we are unable to mitigate risks associated with the 747 and 787 programs, or if we are required

to change one or more of our pricing, cost or other assumptions related to these programs, we could be

required to record reach-forward losses which could have a material effect on our reported results.