UPS 2004 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2004 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

|

|

62 UPS Annual Report 2004

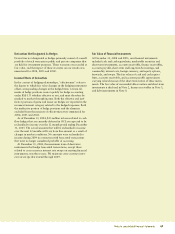

Notes to consolidated financial statements

The IRS had proposed adjustments, unrelated to the EV pack-

age insurance matters discussed above, regarding the allowance

of deductions and certain losses, the characterization of expenses

as capital rather than ordinary, the treatment of certain income,

and our entitlement to tax credits in the 1985 through 1998 tax

years. In the third quarter of 2004, we settled all outstanding

issues related to each of the tax years 1991 through 1998. In the

fourth quarter of 2004, we received a refund of $425 million

pertaining to the 1991 through 1998 tax years. We expect to

receive the $371 million of refunds related to the 1985 through

1990 tax years within the next six months.

The IRS may take similar positions with respect to some of

the non-EV package insurance matters for each of the years

1999 through 2004. If challenged, we expect that we will prevail

on substantially all of these issues. Specifically, we believe that

our practice of expensing the items that the IRS alleges should

have been capitalized is consistent with the practices of other

industry participants. We believe that the eventual resolution of

these issues will not have a material adverse effect on our finan-

cial condition, results of operations or liquidity.

We were named as a defendant in twenty-three now-dis-

missed lawsuits that sought to hold us liable for the collection

of premiums for EV insurance in connection with package ship-

ments since 1984. Based on state and federal tort, contract and

statutory claims, these cases generally claimed that we failed to

remit collected EV premiums to an independent insurer; we

failed to provide promised EV insurance; we acted as an insurer

without complying with state insurance laws and regulations;

and the price for EV insurance was excessive. These actions

were all filed after the August 9, 1999 U.S. Tax Court decision,

discussed above, which the U.S. Court of Appeals for the

Eleventh Circuit later reversed.

These twenty-three cases were consolidated for pre-trial pur-

poses in a multi-district litigation proceeding (“MDL

Proceeding”) in federal court in New York. In addition to the

cases in which UPS was named as a defendant, there also was an

action, Smith v. Mail Boxes Etc., against Mail Boxes Etc. and its

franchisees relating to UPS EV insurance and related services

purchased through Mail Boxes Etc. centers. That case also was

consolidated into the MDL Proceeding.

In late 2003, the parties reached a global settlement resolving

all claims and all cases in the MDL proceeding. In reaching the

settlement, we and the other defendants expressly denied any

and all liability. On July 30, 2004, the court issued an order

granting final approval to the substantive terms of the settle-

ment. No appeals were filed and the settlement became effective

on September 8, 2004.

Pursuant to the settlement, UPS has provided qualifying settle-

ment class members with vouchers toward the purchase of

specified UPS services and will pay the plaintiffs’ attorneys’ fees,

the total amount of which still remains to be determined by the

court. Other defendants have contributed to the costs of the settle-

ment, including the attorneys’ fees. The ultimate cost to us of the

proposed settlement will depend on a number of factors, including

how many vouchers settlement class members actually use. We do

not believe that this proposed settlement will have a material effect

on our financial condition, results of operations, or liquidity.

We are a defendant in a number of lawsuits filed in state

courts containing various class-action allegations under state

wage-and-hour laws. In one of these cases, Marlo v. UPS, which

has been certified as a class action in California state court,

plaintiffs allege that they improperly were denied overtime,

penalties for missed meal and rest periods, interest and attor-

neys’ fees. Plaintiffs purport to represent a class of 1,200

full-time supervisors.

We have denied any liability with respect to these claims and

intend to vigorously defend ourselves in these cases. At this time,

we have not determined the amount of any liability that may

result from these matters or whether such liability, if any, would

have a material adverse effect on our financial condition, results

of operations, or liquidity.

In addition, we are a defendant in various other lawsuits that

arose in the normal course of business. We believe that the even-

tual resolution of these cases will not have a material adverse

effect on our financial condition, results of operations, or liquidity.

We participate in a number of trustee-managed multi-

employer pension and health and welfare plans for employees

covered under collective bargaining agreements. Several factors

could result in potential funding deficiencies which could cause

us to make significantly higher future contributions to these

plans, including unfavorable investment performance, changes in

demographics, and increased benefits to participants. At this

time, we are unable to determine the amount of additional

future contributions, if any, or whether any material adverse

effect on our financial condition, results of operations, or cash

flows could result from our participation in these plans.

NOTE 11. CAPITAL STOCK AND STOCK-BASED

COMPENSATION

Capital Stock

We maintain two classes of common stock, which are distin-

guished from each other by their respective voting rights. Class

A shares of UPS are entitled to 10 votes per share, whereas Class

B shares are entitled to one vote per share. Class A shares are

primarily held by UPS employees and retirees, and these shares

are fully convertible into Class B shares at any time. Class B