UPS 2004 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2004 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

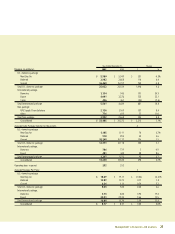

Management’s discussion and analysis 35

These twenty-three cases were consolidated for pre-trial pur-

poses in a multi-district litigation proceeding (“MDL

Proceeding”) in federal court in New York. In addition to the

cases in which UPS was named as a defendant, there also was an

action, Smith v. Mail Boxes Etc., against Mail Boxes Etc. and its

franchisees relating to UPS EV insurance and related services

purchased through Mail Boxes Etc. centers. That case also was

consolidated into the MDL Proceeding.

In late 2003, the parties reached a global settlement resolving

all claims and all cases in the MDL proceeding. In reaching the

settlement, we and the other defendants expressly denied any

and all liability. On July 30, 2004, the court issued an order

granting final approval to the substantive terms of the settle-

ment. No appeals were filed and the settlement became effective

on September 8, 2004.

Pursuant to the settlement, UPS has provided qualifying settle-

ment class members with vouchers toward the purchase of

specified UPS services and will pay the plaintiffs’ attorneys’ fees,

the total amount of which still remains to be determined by the

court. Other defendants have contributed to the costs of the settle-

ment, including the attorneys’ fees. The ultimate cost to us of the

proposed settlement will depend on a number of factors, including

how many vouchers settlement class members actually use. We do

not believe that this proposed settlement will have a material effect

on our financial condition, results of operations, or liquidity.

We are a defendant in a number of lawsuits filed in state

courts containing various class-action allegations under state

wage-and-hour laws. In one of these cases, Marlo v. UPS, which

has been certified as a class action in California state court,

plaintiffs allege that they improperly were denied overtime,

penalties for missed meal and rest periods, interest and attor-

neys’ fees. Plaintiffs purport to represent a class of 1,200

full-time supervisors.

We have denied any liability with respect to these claims and

intend to vigorously defend ourselves in these cases. At this time,

we have not determined the amount of any liability that may

result from these matters or whether such liability, if any, would

have a material adverse effect on our financial condition, results

of operations, or liquidity.

In addition, we are a defendant in various other lawsuits that

arose in the normal course of business. We believe that the even-

tual resolution of these cases will not have a material adverse

effect on our financial condition, results of operations, or liquidity.

We participate in a number of trustee-managed multi-

employer pension and health and welfare plans for employees

covered under collective bargaining agreements. Several factors

could result in potential funding deficiencies which could cause

us to make significantly higher future contributions to these

plans, including unfavorable investment performance, changes in

demographics, and increased benefits to participants. At this

time, we are unable to determine the amount of additional

future contributions, if any, or whether any material adverse

effect on our financial condition, results of operations, or cash

flows could result from our participation in these plans.

Due to the events of September 11, 2001, increased security

requirements for air carriers may be forthcoming; however, we

do not anticipate that such measures will have a material adverse

effect on our financial condition, results of operations, or liquid-

ity. In addition, our insurance premiums have risen and we have

taken several actions, including self-insuring certain risks, to mit-

igate the expense increase.

As of December 31, 2004, we had approximately 229,000

employees employed under a national master agreement and

various supplemental agreements with local unions affiliated

with the International Brotherhood of Teamsters (“Teamsters”).

These agreements run through July 31, 2008. The majority of

our pilots are employed under a collective bargaining agreement

with the Independent Pilots Association, which became amend-

able January 1, 2004. Negotiations are ongoing with the

assistance of the National Mediation Board. Our airline

mechanics are covered by a collective bargaining agreement

with Teamsters Local 2727, which becomes amendable on

November 1, 2006. In addition, the majority of our ground

mechanics who are not employed under agreements with the

Teamsters are employed under collective bargaining agreements

with the International Association of Machinists and Aerospace

Workers. These agreements run through July 31, 2009.

Market Risk

We are exposed to market risk from changes in certain commod-

ity prices, foreign currency exchange rates, interest rates, and

equity prices. All of these market risks arise in the normal course

of business, as we do not engage in speculative trading activities.

In order to manage the risk arising from these exposures, we uti-

lize a variety of foreign exchange, interest rate, equity and

commodity forward contracts, options, and swaps.

The following analysis provides quantitative information

regarding our exposure to commodity price risk, foreign cur-

rency exchange risk, interest rate risk, and equity price risk.

We utilize valuation models to evaluate the sensitivity of the fair

value of financial instruments with exposure to market risk that

assume instantaneous, parallel shifts in exchange rates, interest

rate yield curves, and commodity and equity prices. For options

and instruments with non-linear returns, models appropriate to

the instrument are utilized to determine the impact of market

shifts. There are certain limitations inherent in the sensitivity

analyses presented, primarily due to the assumption that

exchange rates change in a parallel fashion and that interest

rates change instantaneously. In addition, the analyses are

unable to reflect the complex market reactions that normally

would arise from the market shifts modeled.