UPS 2004 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2004 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

50 UPS Annual Report 2004

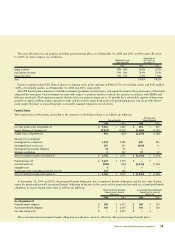

Notes to consolidated financial statements

Derivative Instruments

Derivative instruments are accounted for in accordance

with FASB Statement No. 133, “Accounting for Derivative

Instruments and Hedging Activities” (“FAS 133”), as amended,

which requires all financial derivative instruments to be recorded

on our balance sheet at fair value. Derivatives not designated as

hedges must be adjusted to fair value through income. If a deriv-

ative is designated as a hedge, depending on the nature of the

hedge, changes in its fair value that are considered to be effec-

tive, as defined, either offset the change in fair value of the

hedged assets, liabilities, or firm commitments through income,

or are recorded in OCI until the hedged item is recorded in

income. Any portion of a change in a derivative’s fair value that

is considered to be ineffective, or is excluded from the measure-

ment of effectiveness, is recorded immediately in income.

New Accounting Pronouncements

In December 2004, the FASB issued Statement No. 123 (revised

2004), “Share-Based Payment” (“FAS 123R”), which replaces

FAS 123 and supercedes APB 25. FAS 123R requires all share-

based payments to employees, including grants of employee

stock options, to be recognized in the financial statements based

on their fair values, beginning with the first interim or annual

period after June 15, 2005, with early adoption encouraged.

We will adopt FAS 123R in the third quarter of 2005, using the

prospective method of adoption. The prospective method

requires that compensation expense be recorded for all unvested

stock options and restricted stock at the beginning of the first

quarter of adoption of FAS 123R. There will be no impact upon

adoption, as we will already be expensing all unvested option

and restricted stock awards.

In December 2004, the FASB issued FASB Staff Position

(“FSP”) No. 109-2, “Accounting and Disclosure Guidance for

the Foreign Earnings Repatriation Provision within the

American Jobs Creation Act of 2004” (“FSP 109-2”). FSP 109-2

provides guidance under FAS 109 with respect to recording the

potential impact of the repatriation provisions of the American

Jobs Creation Act of 2004 (the “Jobs Act”) on enterprises’

income tax expense and deferred tax liability. The Jobs Act was

enacted on October 22, 2004. FSP 109-2 states that an enter-

prise is allowed time beyond the financial reporting period of

enactment to evaluate the effect of the Jobs Act on its plan for

reinvestment or repatriation of foreign earnings for purposes of

applying FAS 109. We have not yet completed our evaluation of

the impact of the repatriation provisions of the Jobs Act.

Accordingly, as provided for in FSP 109-2, we have not adjusted

our income tax provision or deferred tax liabilities to reflect the

repatriation provisions of the Jobs Act.

The adoption of the following recent accounting pronounce-

ments did not have a material impact on our results of

operations or financial condition:

nFASB Interpretation No. 45, “Guarantor’s Accounting and

Disclosure Requirements for Guarantees, Including Indirect

Guarantees of Indebtedness of Others — An Interpretation

of FASB Statements No. 5, 57, and 107 and Rescission of

FASB Interpretation No. 34”;

nFASB Interpretation No. 46(R), “Consolidation of Variable

Interest Entities — An Interpretation of ARB No. 51”;

nFASB Statement No. 132(R) (revised 2003), “Employer’s

Disclosures about Pensions and Other Post-Retirement

Benefits — An Amendment of FASB Statements No. 87, 88,

and 106”;

nFASB Statement No. 146, “Accounting for Costs Associated

with Exit or Disposal Activities”;

nFASB Statement No. 149, “Amendment of Statement 133

on Derivative Instruments and Hedging Activities”;

nFASB Statement No. 150, “Accounting for Certain

Instruments with Characteristics of Both Liabilities and

Equity”; and

nFSP 106-2, “Accounting and Disclosure Requirements

Related to the Medicare Prescription Drug, Improvement

and Modernization Act of 2003”.

Changes in Presentation

Certain prior year amounts have been reclassified to conform to

the current year presentation.