UPS 2004 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2004 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

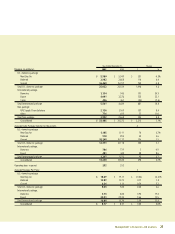

36 UPS Annual Report 2004

Management’s discussion and analysis of financial condition and results of operations

A discussion of our accounting policies for derivative instru-

ments and further disclosures are provided in Note 16 to the

consolidated financial statements.

Commodity Price Risk

We are exposed to an increase in the prices of refined fuels, prin-

cipally jet-A, diesel, and unleaded gasoline, which are used in the

transportation of packages. Additionally, we are exposed to an

increase in the prices of other energy products, primarily natural

gas and electricity, used in our operating facilities throughout the

world. We use a combination of options, swaps, and futures

contracts to provide some protection from rising fuel and energy

prices. These derivative instruments generally cover forecasted

fuel and energy consumption for periods of one to three years.

The net fair value of such contracts subject to price risk, exclud-

ing the underlying exposures, as of December 31, 2004 and

2003 was an asset of $101 and $30 million, respectively. The

potential loss in the fair value of these derivative contracts,

assuming a hypothetical 10% change in the underlying commod-

ity price, would be approximately $32 and $17 million at

December 31, 2004 and 2003, respectively. This amount

excludes the offsetting impact of the price risk inherent in the

physical purchase of the underlying commodities.

Foreign Currency Exchange Risk

We have foreign currency risks related to our revenue, operating

expenses, and financing transactions in currencies other than the

local currencies in which we operate. We are exposed to currency

risk from the potential changes in functional currency values of

our foreign currency-denominated assets, liabilities, and cash

flows. Our most significant foreign currency exposures relate to

the Euro, the British Pound Sterling and the Canadian Dollar. We

use a combination of purchased and written options and forward

contracts to hedge cash flow currency exposures. These derivative

instruments generally cover forecasted foreign currency exposures

for periods up to one year. As of December 31, 2004 and 2003,

the net fair value of the hedging instruments described above was

a liability of $(28) and $(48) million, respectively. The potential

loss in fair value for such instruments from a hypothetical 10%

adverse change in quoted foreign currency exchange rates would

be approximately $117 and $97 million at December 31, 2004

and 2003, respectively. This sensitivity analysis assumes a parallel

shift in the foreign currency exchange rates. Exchange rates rarely

move in the same direction. The assumption that exchange rates

change in a parallel fashion may overstate the impact of changing

exchange rates on assets and liabilities denominated in a foreign

currency.

Interest Rate Risk

As described in Note 8 to the consolidated financial statements,

we have issued debt instruments, including debt associated with

capital leases, that accrue expense at fixed and floating rates of

interest. We use a combination of derivative instruments, includ-

ing interest rate swaps and cross-currency interest rate swaps, as

part of our program to manage the fixed and floating interest

rate mix of our total debt portfolio and related overall cost of

borrowing. These swaps are generally entered into concurrently

with the issuance of the debt that they are intended to modify,

and the notional amount, interest payment, and maturity dates

of the swaps match the terms of the associated debt.

Our floating rate debt and interest rate swaps subject us to

risk resulting from changes in short-term (primarily LIBOR)

interest rates. The potential change in annual interest expense

resulting from a hypothetical 100 basis point change in short-

term interest rates applied to our floating rate debt and swap

instruments at December 31, 2004 and 2003 would be approxi-

mately $29 and $25 million, respectively.

As described in Note 1 and Note 2 to the consolidated finan-

cial statements, we have certain investments in debt, auction

rate, and preferred securities that accrue income at variable rates

of interest. The potential change in annual investment income

resulting from a hypothetical 100 basis point change in interest

rates applied to our investments exposed to variable interest

rates at December 31, 2004 and 2003 would be approximately

$45 and $31 million, respectively.

Additionally, as described in Note 3 to the consolidated finan-

cial statements, we hold a portfolio of finance receivables that

accrue income at fixed and floating rates of interest. The poten-

tial change in the annual income resulting from a hypothetical

100 basis point change in interest rates applied to our variable

rate finance receivables at December 31, 2004 and 2003 would

be immaterial.

This interest rate sensitivity analysis assumes interest rate

changes are instantaneous, parallel shifts in the yield curve. In

reality, interest rate changes are rarely instantaneous or parallel.

While this is our best estimate of the impact of the specified

interest rate scenarios, these estimates should not be viewed as

forecasts. We adjust the fixed and floating interest rate mix of

our interest rate sensitive assets and liabilities in response to

changes in market conditions.

Equity Price Risk

We hold investments in various common equity securities that

are subject to price risk, and for certain of these securities, we

utilize options to hedge this price risk. At December 31, 2004

and 2003, the fair value of such investments was $77 and $95

million, respectively. The potential change in the fair value of

such investments, assuming a 10% change in equity prices net

of the offsetting impact of any hedges, would be approximately

$8 and $10 million at December 31, 2004 and 2003.