Thrifty Car Rental 2009 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2009 Thrifty Car Rental annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

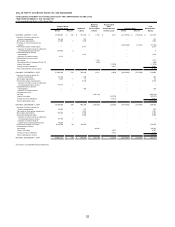

|

|

received directly from auctions, with any shortfall in value being paid by the vehicle manufacturer.

With certain other vehicle manufacturers, the entire balance of proceeds from vehicle sales comes

directly from the manufacturer. In either case, the Company bears the risk of collectibility on the

receivable from the vehicle manufacturer. The Company monitors its vehicle manufacturer

receivables based on time outstanding, manufacturer strength and length of the relationship.

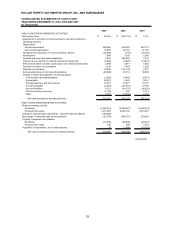

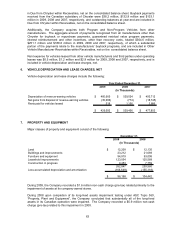

Property and Equipment – Property and equipment are recorded at cost and are depreciated using

principally the straight-line method over the estimated useful lives of the related assets. Estimated

useful lives generally range from ten to thirty years for buildings and improvements and three to

seven years for furniture and equipment. Leasehold improvements are amortized over the estimated

useful lives of the related assets or leases, whichever is shorter.

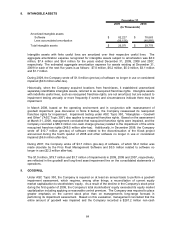

Intangible Assets – Software is recorded at cost and amortized using the straight-line method

primarily over five years. The remaining useful life of all intangible assets is evaluated annually to

assess whether events and circumstances warrant a revision to the remaining amortization period.

Reacquired franchise rights, established upon reacquiring a previously franchised location, are not

amortized as they have an indefinite life, rather they are tested annually for impairment (Note 8).

Website Development Costs – The Company capitalizes qualifying internal-use software

development, including Website development, incurred subsequent to the completion of the

preliminary project stage. Development costs are amortized over the shorter of the expected useful

life of the software or five years. Costs related to planning, maintenance, and minor upgrades are

expensed as incurred.

Goodwill – The excess of acquisition costs over the fair value of net assets acquired is recorded as

goodwill. Goodwill is tested for impairment at least annually (Note 9).

Long–Lived Assets – The Company reviews the value of long-lived assets, including software and

other intangible assets, for impairment whenever events or changes in circumstances indicate that

the carrying amount of an asset may not be recoverable based upon estimated future cash flows.

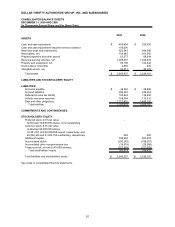

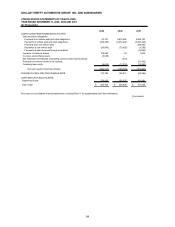

Accounts Payable – Book overdrafts of $20.5 million and $7.6 million, which represent outstanding

checks not yet presented to the bank, are included in accounts payable at December 31, 2009 and

2008, respectively. These amounts do not represent bank overdrafts, which would constitute

checks presented in excess of cash on hand, and would be effectively a loan to the Company.

Derivative Instruments – The Company records all derivatives on the balance sheet as either

assets or liabilities measured at their fair value, and changes in the derivatives’ fair value are

recognized currently in earnings unless specific hedge accounting criteria are met. In 2005 and

2006, the Company entered into interest rate swap agreements, which do not qualify for hedge

accounting treatment; therefore, the changes in the interest rate swap agreements’ fair values have

been recognized as an (increase) decrease in fair value of derivatives in the consolidated statement

of operations. In May 2007, the Company entered into an interest rate swap agreement related to

the 2007 Series notes (hereinafter defined) which constitutes a cash flow hedge and qualifies for

hedge accounting treatment; therefore, changes in fair value are recorded in accumulated other

comprehensive loss (Note 11).

Vehicle Insurance Reserves – Provisions for public liability and property damage and

supplemental liability insurance (“SLI”) on self-insured claims are made by charges primarily to

direct vehicle and operating expense. Accruals for such charges are based upon actuarially

determined evaluations of estimated ultimate liabilities on reported and unreported claims, prepared

on at least an annual basis. Historical data related to the amount and timing of payments for self-

insured claims is utilized in preparing the actuarial evaluations. The accrual for public liability and

property damage claims is discounted based upon the actuarially determined estimated timing of

payments to be made in the future. Management reviews the actual timing of payments as

compared with the annual actuarial estimate of timing of payments and has determined that there

57